October was a pivotal month for global markets, marked by a series of geopolitical and economic developments that reshaped investor sentiment.

The most prominent was the ceasefire between Hamas and Israel, paired with fresh U.S. sanctions on Russia’s two largest oil companies, Lukoil and Rosneft.

The move heightened pressure on Moscow as U.S. President Donald Trump appeared to lose patience with Vladimir Putin and the ongoing war in Ukraine.

Elsewhere, trade tensions between the U.S. and China resurfaced early in the month when Trump threatened to impose 100% tariffs on Chinese goods in response to Beijing’s export controls on critical minerals.

However, the tone quickly shifted after Trump and President Xi Jinping met in Asia, calling the encounter a “12 out of 10.” The two leaders agreed to a trade framework, including a temporary suspension of tariffs and commitments for new agricultural purchases — sparking optimism across global markets.

Meanwhile, the U.S. government shutdown, now extending through its fifth week, continues to restrict the release of crucial economic data. Despite this, the Federal Reserve proceeded with a 25-basis-point rate cut, its first since June, while Chair Jerome Powell adopted a measured tone, stressing that future policy decisions will remain data dependent.

The decision came alongside a slightly cooler inflation print, bolstering confidence that further easing could follow if disinflation persists.

In commodities, gold briefly surged above $4,000/oz before recording its sharpest one-day drop in over a decade, while oil prices rebounded from yearly lows after sanctions reduced Russian supply.

Forex

Global growth concerns and rising safe-haven demand supported the U.S. dollar through much of October, although gains were capped by uncertainty surrounding the government shutdown.

The softer CPI data increased speculation that the Fed could deliver additional cuts, which could later weigh on the dollar.

The euro weakened as the ECB continued to balance the difficult trade-off between supporting growth and managing inflation. After a strong 2025 performance, the EURUSD pair entered a mild correction phase, with traders closely monitoring upcoming inflation and labour market data for directional cues.

Fig. 1: Four-hour EURUSD chart showing continuation of the downward channel amid sustained USD strength in October.

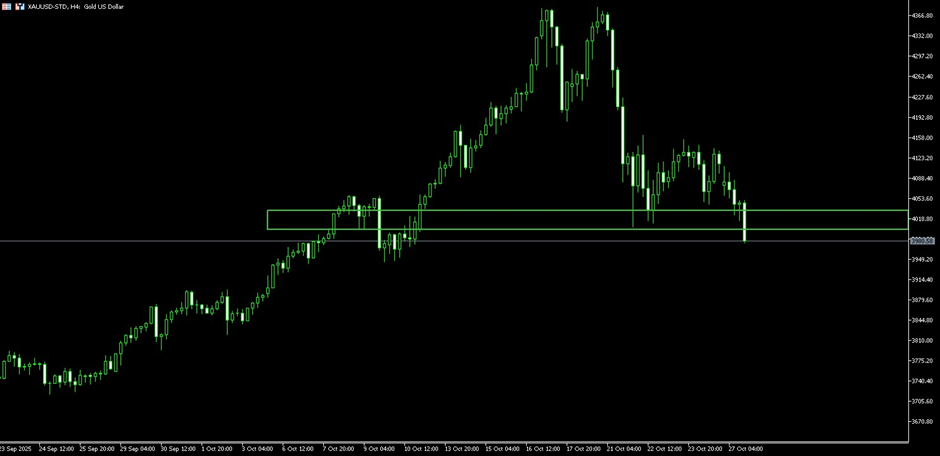

Gold

Gold and silver both climbed to record highs in October, with gold breaching the $4,000/oz mark to peak around $4,380, while silver rallied above $50/oz, hitting $54.40.

Since those peaks, both metals have seen healthy corrections. Gold’s sharp one-day drop on 21 October marked its steepest decline in more than a decade. However, the core bullish fundamentals remain intact — lingering geopolitical risks, inflation uncertainty, and strong central bank demand continue to underpin the broader trend.

The recent pullback looks more like a technical correction and profit-taking phase, supported by easing tensions and a temporary return to risk-on sentiment.

Fig. 2: Four-hour gold chart showing its breakout above $4,000/oz before retreating toward the end of the month.

Oil

Oil prices came under pressure early in October, sliding towards yearly lows near $56 per barrel as OPEC+ continued to unwind production cuts and non-OPEC producers like the U.S., Brazil, and Canada ramped up output. Softer demand further compounded fears of oversupply, driving prices lower.

The situation reversed mid-month after the U.S. imposed sanctions on Lukoil and Rosneft, prompting some Asian buyers to scale back Russian oil imports for fear of secondary sanctions. This effectively reduced near-term supply, lifting prices off their lows.

However, analysts expect the rebound may be short-lived if sanctions achieve their intended goal — bringing Russia back to the negotiating table to end the Ukraine conflict.

Fig. 3: Four-hour oil chart showing early-month weakness followed by a rebound on U.S. sanctions against Russian energy companies.

Crypto

Bitcoin experienced heightened volatility through October but remains structurally stable within its broader range. The cryptocurrency hit a new all-time high above $125,000 early in the month, only to see a wave of derivative liquidations trigger a sharp sell-off.

Prices have since stabilised, with improved risk sentiment and easing geopolitical tensions helping BTC recover towards the $115,000 zone from lows just below $104,000.

Fig. 4: Daily Bitcoin chart showing October volatility while maintaining the broader bullish structure.

Indices

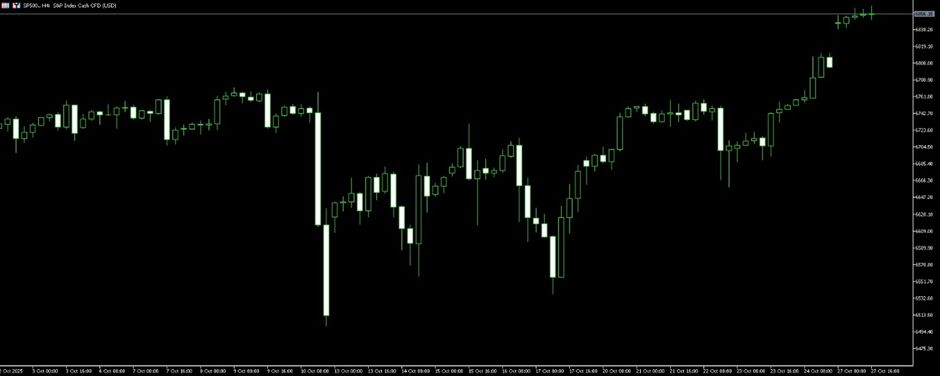

U.S. equities opened in October with a sharp pullback amid fears of a renewed U.S.–China trade war. Sentiment quickly stabilised after Trump stated that Washington seeks to “work with China, not against it.”

Markets rallied after Treasury Secretary Scott Bessent announced that both nations had agreed to a trade deal framework, ahead of the expected Trump–Xi meeting in South Korea. The S&P 500 has since rallied to fresh record highs ahead of key tech earnings.

Elsewhere, European indices followed suit, with the FTSE reaching new highs, while in Asia, both the Nikkei and ASX marked record levels. China’s A50 Index also surged to its highest point in a year following renewed optimism around trade negotiations.

Fig. 5: Four-hour S&P 500 chart showing the initial sell-off on trade war fears and the subsequent gap-up rally after the U.S.–China deal framework announcement.

Market Playbook: The Trader’s Game Plan for November

With U.S. indices at record highs, a fresh Fed rate cut, and easing U.S.–China tensions, traders are entering November with renewed optimism but also elevated risk.

Why U.S. Indices Hit Record Highs

The rally was fuelled by three converging catalysts:

- Monetary easing, as the Fed’s 25 bps cut reignited liquidity hopes.

- Trade stability, with the Trump–Xi framework removing a key overhang for risk assets.

- Corporate earnings, which continued to outperform expectations, particularly in tech and banking sectors.

The result: stronger breadth across equities and a surge in global risk appetite.

Impact of the Rate Cut

The Fed’s decision has reinforced the view that policy is turning supportive again, driving capital into growth-sensitive sectors such as technology, consumer discretionary, and financials.

However, Powell’s cautionary tone implies future moves will hinge on incoming data, leaving room for volatility if inflation or employment data surprise to the upside.

Strategy and Ideas

Traders can look to stay long on dips in leading indices or rotate into sectors that benefit from lower rates. Growth names, high-multiple tech stocks, and interest-sensitive assets are likely to outperform if the rate-cut trajectory continues.

Those seeking tactical exposure might also consider options strategies to capture potential upside while limiting downside in case sentiment shifts.

Risk Awareness

Valuations are stretched, and with optimism priced in, any data disappointment or geopolitical flare-up could trigger outsized reactions. Traders should monitor inflation prints, labour data, and Fed commentary closely for early signals of a sentiment turn.

Position sizing, hedging, and selective profit-taking will be crucial to navigating elevated markets without overexposure.

Into November

For the month ahead, the best approach is a balanced one— maintain exposure to growth while managing risk proactively.

- Watch for follow-through on trade progress. If talks stall, risk assets could retrace quickly.

- Monitor inflation and jobs data for clues on the Fed’s next steps.

- Scale into strength cautiously, booking profits on spikes and re-entering on pullbacks.

In short, November presents both opportunity and risk: a supportive policy backdrop with markets already priced for perfection. The traders who combine conviction with discipline will be best positioned for what’s next.