On Wednesday, the S&P 500 closed at 4,186.77, dipping below the critical 4,200 level, spurred by Alphabet’s disappointing earnings, tech stock declines, and rising bond yields. Microsoft bucked the trend with a 3% share price increase after strong earnings. Meanwhile, in the currency market, the US dollar gained ground due to higher Treasury yields, while major currencies like the euro and pound struggled. The yen faced a make-or-break moment against the dollar, and the Canadian dollar hit mid-March highs following the Bank of Canada’s cautious stance. Upcoming economic data releases and the ECB meeting are poised to impact the financial landscape further.

On Wednesday, the S&P 500 experienced a significant decline, closing at 4,186.77, which was below a key level of 4,200. This drop of 1.43% marked the first time the S&P 500 had closed below this level since May, a development closely monitored by chart analysts. The downward trend was attributed to disappointing quarterly results from Alphabet, the parent company of Google, which saw its shares plummet more than 9% due to a miss in its cloud business performance, overshadowing otherwise strong revenue growth and earnings. The S&P 500’s communication services sector also took a hit, losing 5.9%. Other major tech giants, such as Apple and Amazon, saw their shares decline by 1.3% and 5.6%, respectively. Concerns also revolved around rising bond yields, with the 10-year Treasury yield spiking nearly 11 basis points to approximately 4.95%, causing jitters in the market and negatively impacting tech stocks.

Amid this turbulence, Microsoft stood out as an exception among tech stocks, experiencing a 3% increase in share prices after it posted fiscal first-quarter results that exceeded Wall Street expectations. Additionally, other tech firms like IBM and Meta were set to announce their quarterly results in the afternoon. So far, approximately 29% of S&P 500 companies have reported their third-quarter earnings and an impressive 78% of these companies have surpassed analysts’ expectations. While corporate earnings remained a focal point for investors, the bond market’s rapid rise in yields, not witnessed since 1982, raised concerns about the future of the stock market.

Data by Bloomberg

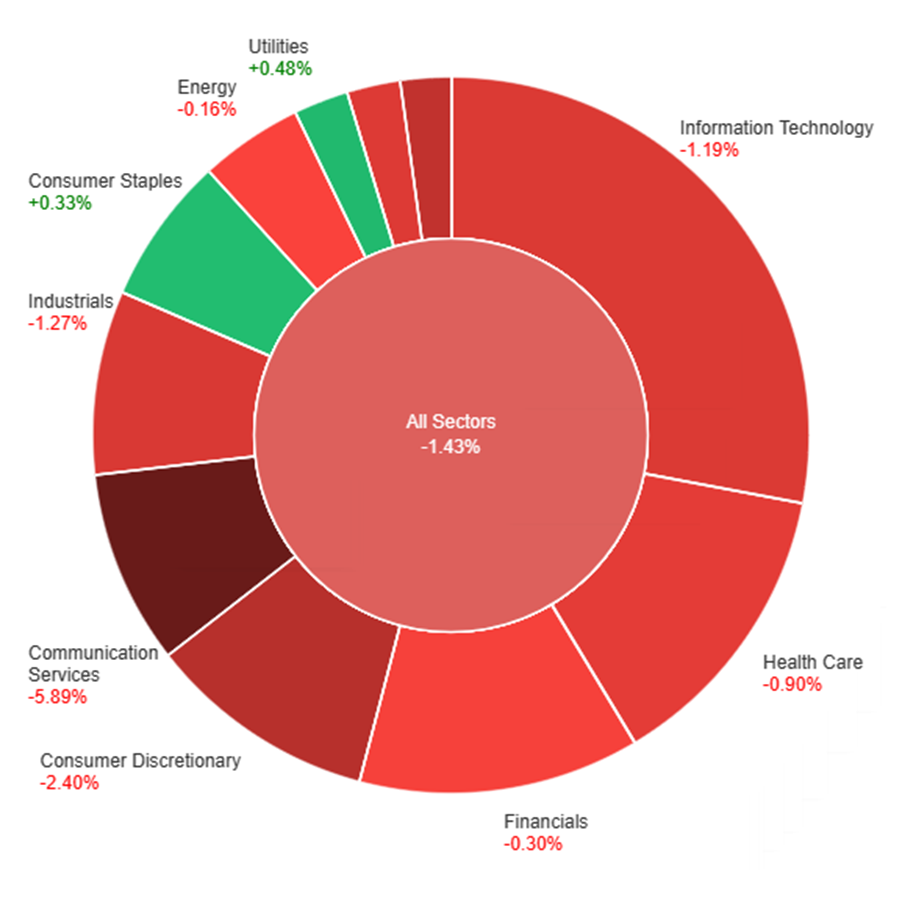

On Wednesday, various sectors experienced different changes in their stock market performance. Overall, the All Sectors index decreased by 1.43%. The sectors of Utilities and Consumer Staples showed modest gains, with increases of 0.48% and 0.33%, respectively. On the other hand, several sectors saw declines: Energy (-0.16%), Financials (-0.30%), Health Care (-0.90%), Materials (-1.14%), Information Technology (-1.19%), Industrials (-1.27%), Real Estate (-2.07%), Consumer Discretionary (-2.40%), and Communication Services (-5.89%) all faced negative returns.

In the latest currency market updates, the US dollar saw a 0.2% rise, primarily driven by risk-off sentiment and higher Treasury yields when compared to the yields of bunds, gilts, and JGBs, which favored the safety of the US currency. Notably, the EUR/USD pair struggled to gain momentum despite better-than-expected German Ifo data and the lowest MBA mortgage purchase reading in the US since 1995. Weak lending data in the eurozone raised concerns of a looming recession, while the US exhibited a strong rebound. Additionally, falling US stocks, a return of 10-year Treasury yields towards the 5% mark, and increasing oil prices all contributed to the dollar’s strength, particularly against currencies sensitive to market risks. The pair, EUR/USD, dropped by 0.2%, reaching its lowest level since the previous Friday. This decline followed a significant bearish rejection from the 50% Fibonacci retracement level and the 55-day moving average resistance.

Furthermore, other major currencies were also impacted by the dollar’s resurgence. The British pound fell by 0.32%, with investors eagerly awaiting further UK inflation data that might confirm the Bank of England’s expectations of a significant year-end drop, potentially leading to interest rate cuts. USD/JPY briefly touched above the 150 mark for the third time in the current month, driven by the widening yield spreads between US Treasuries and Japanese government bonds (JGBs). The relatively shallow pullbacks observed in the market have placed the dollar in a critical make-or-break position, one that could challenge the Japanese Ministry of Finance’s tolerance for further yen depreciation towards the 32-year peak seen in 2022 at 151.94. Meanwhile, the Bank of Japan’s readiness to continue quantitative easing to defend its current 1% 10-year yield cap also remains a crucial factor. In contrast, the Australian dollar experienced a brief rally following unexpectedly strong Q3 inflation figures but subsequently dropped by 0.72% due to risk-off market flows. Lastly, the Chinese yuan depreciated by 0.24% as concerns about local and central government limitations on risk-taking activities overshadowed the effects of modest fiscal stimulus announcements. The USD/CAD pair rose by 0.4% to reach its highest level since mid-March, following the Bank of Canada’s decision to maintain its interest rates and express concerns about the narrowing path to avoid a recession, raising questions about the comparative hawkishness of the Bank of Canada versus the Federal Reserve’s policy pricing. This week’s agenda includes the ECB meeting, which is widely expected to maintain the status quo, followed by significant US economic data releases, such as durable goods, Q3 GDP figures, core PCE data, jobless claims, and pending home sales.

EUR/USD Slides Below 1.0600 as Strong US Dollar Dominates, Eyes on ECB and US Economic Data

The EUR/USD currency pair faced a second consecutive day of declines, dropping below the 1.0600 mark, driven by the strength of the US Dollar. Market attention now shifts to the European Central Bank’s (ECB) upcoming meeting and significant US economic data releases. Notably, the German IFO Business Survey displayed positive results, while the ECB is expected to maintain unchanged interest rates amid concerns about slowing inflation and subdued economic activity. Additionally, robust US economic data could further bolster the US Dollar, while any negative surprises may trigger a correction in the currency pair.

According to technical analysis, the EUR/USD moved lower on Wednesday, approaching the middle band of the Bollinger Bands. Currently, the EUR/USD is trading between the middle and lower bands, indicating the potential for further downward movement. The Relative Strength Index (RSI) is at 39, signaling that the EUR/USD is adopting a bearish bias.

Resistance: 1.0616, 1.0705

Support: 1.0500, 1.0405

XAU/USD Climbs to $1,982 as Markets Weigh Economic Outlook Amidst Earnings Season and Central Bank Decisions

In Wednesday’s trading, XAU/USD made gains, reaching approximately $1,982 per troy ounce. As financial markets closely observe Wall Street’s earnings reports, the focus is on the economic outlook leading up to pivotal events on Thursday. Anticipations of robust U.S. economic growth, potentially at an annualized rate of 4.2% for the third quarter, are raising questions about interest rates and the Federal Reserve’s stance. Simultaneously, the European Central Bank (ECB) is expected to maintain rates and adopt a cautious approach to future monetary policy. Earnings season is further impacting sentiment, with mixed results from major tech companies affecting stock indices, and rising government bond yields adding to market dynamics.

According to technical analysis, XAU/USD is consolidating on Wednesday and has the potential to reach the upper band of the Bollinger Bands, which is currently squeezing. Presently, the price of gold is consolidating near the upper band, implying a possible downward consolidation. The Relative Strength Index (RSI) is currently at 60, indicating a neutral bias for the XAU/USD pair.

Resistance: $1,985, $2,002

Support: $1,970, $1,959

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| EUR | Main Refinancing Rate | 20:15 | 4.50% |

| EUR | Monetary Policy Statement | 20:15 | |

| USD | Advance GDP q/q | 20:30 | 4.5% |

| USD | Unemployment Claims | 20:30 | 208k |

| EUR | ECB Press Conference | 20:45 |