Key Takeaways

- US GDP exceeded expectations, reinforcing the view that the economy remains resilient despite higher interest rates.

- A stronger economy reduces pressure on the Federal Reserve to cut rates, keeping real yields elevated and weighing on gold.

- Higher Treasury yields and a stronger US dollar increase the opportunity cost of holding non yielding assets such as gold.

- Central bank buying and long term fiscal concerns continue to provide structural support, preventing a sharper decline in gold prices.

- Upcoming inflation data, labour market reports and Fed communications will be the key catalysts that determine gold’s next major move.

The GDP Print That Complicates Gold’s Path

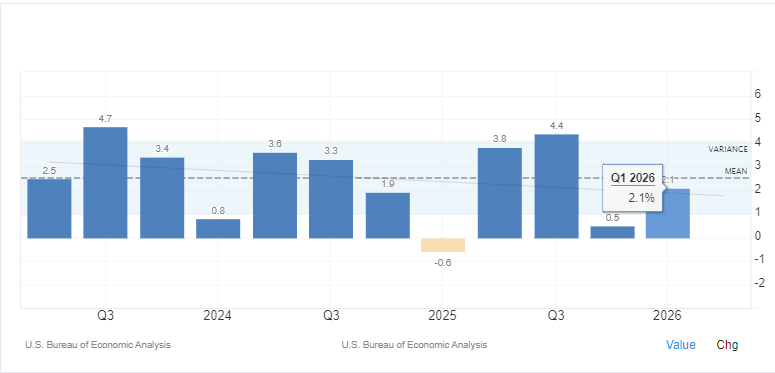

The U.S. Bureau of Economic Analysis released its final Q1 2026 GDP reading this morning at 2.1% annualised, beating market expectations of 1.6% and coming in slightly above the initial estimate of 2.0%. For gold traders, a stronger than expected economy is generally a headwind. Strong economic growth reduces the urgency for the Federal Reserve to cut interest rates, supports higher real yields and weakens the appeal of non yielding assets such as gold. If you’re looking to better understand the factors that influence precious metal, our Ultimate Guide to Gold Investing explores the key drivers behind gold prices and the different ways traders gain exposure to the market.

The stronger GDP figure also reinforces the view that the U.S. economy remains remarkably resilient despite an extended period of restrictive monetary policy. Many investors expected higher borrowing costs to slow consumer spending and business investment more noticeably. Instead, economic activity has continued to outperform expectations. This resilience gives policymakers greater confidence that the economy can withstand higher interest rates for longer.

Gold is currently trading near $4,000 per ounce, roughly 28% below its all time high of $5,589 reached in late January. Although today’s GDP release alone is unlikely to determine gold’s next major move, it strengthens the case for a higher for longer interest rate environment.

The Fed Hold Is Still the Key Variable

Gold’s relationship with GDP is not direct. Instead, it is largely driven by how the Federal Reserve responds to economic conditions.

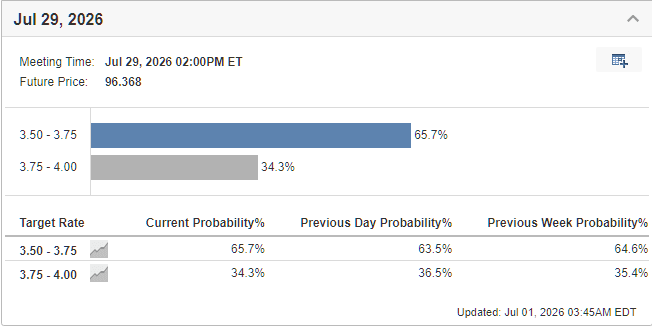

A stronger economy gives the Fed greater flexibility to leave interest rates unchanged or even tighten policy further if inflation remains persistent. With headline PCE inflation running at 3.8% year on year and core PCE at 3.3%, the Fed, under Chair Kevin Warsh, has continued to signal a cautious approach towards easing monetary policy.

Markets are now pricing roughly a 70% probability of at least one rate hike by December, reflecting growing confidence that policymakers are unlikely to pivot towards rate cuts any time soon. For gold investors, this matters because expectations surrounding interest rates have historically been one of the most important drivers of gold prices.

Why Higher Rates Weigh on Gold

Unlike bonds or savings accounts, gold does not generate any income. Its attractiveness depends largely on the opportunity cost of holding it.

When Treasury yields rise, investors can earn higher returns by holding government bonds, making non-yielding assets such as gold less attractive. Real yields, which measure returns after adjusting for inflation, are particularly important because they reflect the true purchasing power investors receive from fixed income assets. To compare asset structures directly, check out our Gold vs. S&P 500 Performance Guide to see how precious metals stack up against yield-bearing and equity markets during restrictive cycles.

The U.S. 10-year Treasury Inflation Protected Securities, or TIPS, yield currently stands near 2.234%, remaining close to multi-year highs. As long as real yields remain elevated, gold is likely to face continued pressure.

According to Goldman Sachs, every 25 basis point rate cut could generate approximately 60 tonnes of additional gold ETF demand. Without those expected rate cuts, one of gold’s strongest sources of investment demand remains absent.

A Stronger Dollar Adds Further Pressure

Today’s GDP surprise also supported the U.S. dollar, another important factor for gold traders.

A stronger economy tends to attract foreign investment into U.S. assets, increasing demand for the dollar. Because gold is traded globally against the US dollar as XAU/USD, changes in the strength of the dollar often have a direct impact on price movements. Understanding this relationship is essential for traders looking to navigate the gold market effectively. If you’re unfamiliar with the pair, our guide to XAU/USD trading explains how the gold and US dollar relationship influences trading opportunities.

Historically, gold and the U.S. dollar have shared an inverse relationship. While that relationship is not always perfect, periods of sustained dollar strength have frequently coincided with weaker gold prices, particularly when accompanied by rising real yields.

What Is Preventing Gold From Falling Further?

Despite these macroeconomic headwinds, gold continues to benefit from several structural factors that have prevented a deeper correction.

Central banks purchased an estimated 244 tonnes of gold during the first quarter of 2026, with China extending its reserve accumulation for an eighteenth consecutive month. Unlike speculative investors, central banks are generally less sensitive to short term interest rate movements and instead focus on long term reserve diversification. You can view the macro layout of who holds the most physical metal globally in our analysis of the Top 10 Countries with the Most Gold Reserves.

Fiscal concerns also remain firmly in focus. The U.S. budget deficit continues to run between 6% and 7% of GDP, while annual interest payments are approaching $1 trillion. These longer term debt dynamics continue to raise questions about the sustainability of U.S. fiscal policy and the dollar’s long term purchasing power, providing a structural argument for holding gold regardless of short term economic data. For alternative safe havens facing these same structural questions, see our head-to-head comparison: Bitcoin vs. Gold: Which is the Better Store of Value?.

What Traders Should Watch Next

Although today’s GDP report reinforces the case for a patient Federal Reserve, it is unlikely to be the final piece of the puzzle.

Markets will now turn their attention to upcoming PCE inflation data, Non Farm Payrolls and future FOMC communications. A meaningful slowdown in inflation or signs that the labour market is beginning to weaken could quickly revive expectations for interest rate cuts, providing renewed support for gold. Traders looking to execute strategies around these upcoming macroeconomic data drops can brush up on their approach with our tactical guide on How to Trade Forex on News Releases.

On the other hand, another series of stronger than expected economic releases would reinforce the higher for longer narrative, keeping upward pressure on Treasury yields and limiting gold’s recovery potential. When trading through these highly volatile shifts, setting tight protective boundaries is crucial; make sure you understand risk parameters via our Trade Risk Management Tips.

The Outlook

In the near term, today’s GDP beat strengthens the case for gold to remain under pressure, with the $3,800 to $4,200 region likely to contain price action while the Federal Reserve maintains its cautious stance.

The key catalysts to monitor are signs of weakness in the labour market, softer inflation data or any shift in FOMC communication towards monetary easing. Until then, elevated real yields and a resilient economy are likely to limit upside momentum. For a deeper look into visual trends and technical patterns forming within these boundaries, explore our complete Gold Value Trend and Price Forecast.

That said, the longer term outlook remains constructive. Major financial institutions continue to expect higher gold prices over the coming quarters, with Goldman Sachs forecasting $4,900 by the end of the year and J.P. Morgan targeting $5,000 during the fourth quarter of 2026. The path towards those targets ultimately depends on one key factor, namely the return of expectations for Federal Reserve rate cuts. Today’s stronger GDP report suggests that moment may have been pushed a little further into the future.

For traders looking to take advantage of these macroeconomic developments, having a clear understanding of How to Trade in Gold or utilizing flexible frameworks through Precious Metal CFD Trading can significantly help improve decision-making during periods of heightened market volatility.

The Big Questions

1) Why does a strong US GDP hurt gold prices?

A stronger economy (like the Q1 2026 GDP beating expectations at 2.1%) means the Federal Reserve has less pressure to cut interest rates. Since gold doesn’t pay interest or dividends, higher interest rates make yield-bearing assets like bonds more attractive, reducing the demand for gold.

2) How do rising real yields affect gold (XAU/USD)?

Real yields reflect the actual return investors get from government bonds after adjusting for inflation. When real yields rise, the opportunity cost of holding non-yielding gold increases, putting direct downward pressure on spot prices.

3) What is the relationship between the US dollar and gold?

Gold is priced globally in US dollars (XAU/USD). A strong US economy strengthens the dollar, making gold more expensive for international buyers holding other currencies, which naturally depresses demand.

4) What is keeping gold prices from crashing completely?

Gold is supported by strong structural factors, including massive buying from global institutions—central banks bought 244 tonnes in Q1 2026 alone. Long-term US debt and deficit concerns also preserve gold’s appeal as a hard-asset shield against inflation.

5) What should gold traders watch next for a market pivot?

Traders should closely monitor upcoming PCE inflation data, Non-Farm Payrolls (NFP), and Federal Reserve commentary. Any signs of an economic slowdown or cooling inflation could bring rate cuts back to the table, sparking a recovery for gold.

6) What is the current price outlook for gold?

Prices are expected to face near-term pressure within a consolidation range of $3,800 to $4,200 per ounce. However, long-term forecasts remain highly bullish, with consensus targets sitting between $4,900 and $5,000 once rate cuts begin.