Stocks experienced a renewed downward trend on Tuesday, triggered by a credit rating downgrade of the banking sector from Moody’s in the midst of an August selloff. The Dow Jones Industrial Average closed with a loss of 158.64 points, or 0.45%, settling at 35,314.49, while the S&P 500 ended down 0.42% at 4,499.38, reflecting a month-to-date decline of nearly 2%. The Nasdaq Composite also retreated by 0.79% to 13,884.32, deepening its August loss to 3.2%. This marked the fifth negative day in six sessions for both the S&P 500 and the Nasdaq, with neither index breaking into positive territory despite recovering from session lows.

Moody’s credit rating downgrade had a pronounced impact on the banking sector, causing a broad decline. Regional banks like M&T Bank and Pinnacle Financial faced credit rating reductions due to concerns about deposit risk, potential recession, and challenges in commercial real estate portfolios. Bank of N.Y. Mellon and State Street were placed under review for potential downgrades as well. Consequently, banking giants Goldman Sachs and JPMorgan Chase saw declines of around 2.1% and 0.6%, respectively, while the SPDR S&P Bank ETF (KBE) dropped by 1.3%. The SPDR S&P Regional Banking ETF (KRE) also lost 1.3%, with a notable history of decline due to previous events such as the failure of Silicon Valley Bank. The downgrade emphasized the crucial importance of strong credit ratings for regional banks, as any loss of faith in the sector negatively impacts market sentiment. Amid these developments, UPS reported weaker-than-expected revenue for Q2, leading to a 0.9% drop in its shares. Despite the generally positive corporate earnings season, where a majority of S&P 500 companies exceeded expectations, the market appeared to have already priced in these results, contributing to the ongoing pullback.

Data by Bloomberg

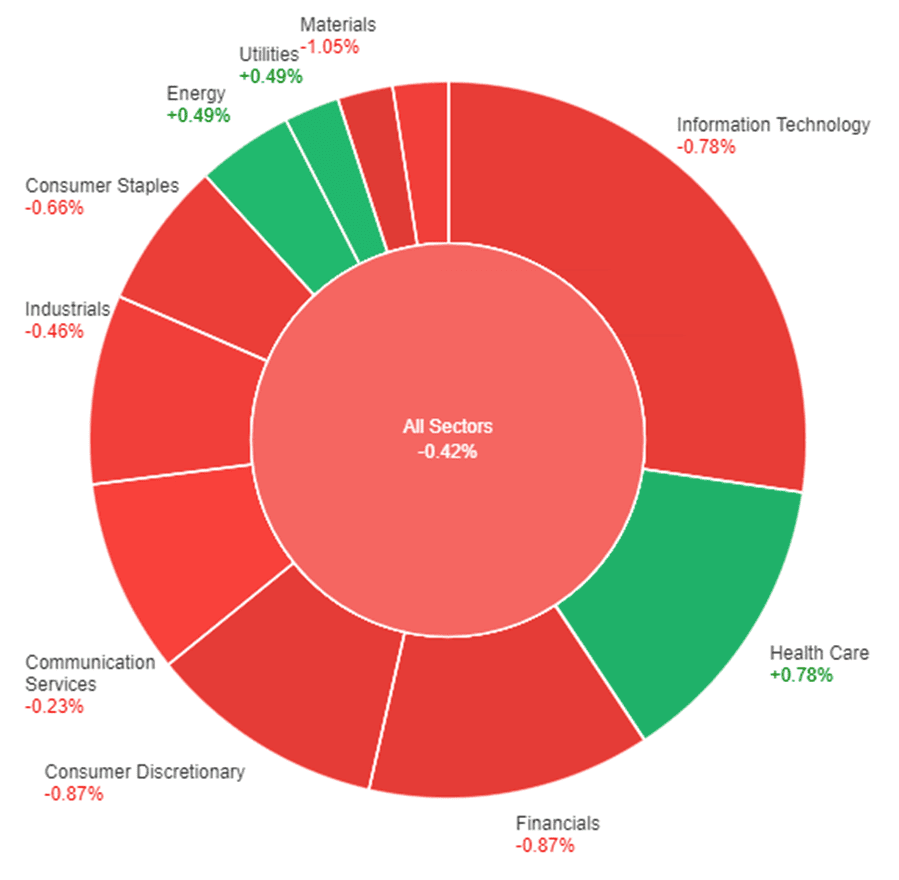

On Tuesday, most sectors experienced a decline, with the overall market decreasing by 0.42%. Health Care and Utilities, however, showed gains, rising by 0.78% and 0.49% respectively. Energy also saw a similar increase of 0.49%. Communication Services and Real Estate sectors faced slight decreases of 0.23% and 0.45% respectively. Industrials, Consumer Staples, Information Technology, and Consumer Discretionary sectors all declined, ranging from -0.46% to -0.87%. Financials and Materials were the hardest hit, both decreasing by 0.87% and 1.05% respectively.

Major Pair Movement

The dollar index exhibited a 0.54% increase on Tuesday, primarily driven by safe-haven demand, which overshadowed even larger gains against currencies sensitive to risk due to recent events. The euro faced additional downward pressure due to its significant reliance on Chinese demand, worsened by recent data. The European Central Bank’s (ECB) struggle to fully address inflation, with both overall and core euro zone inflation remaining above 5%, has led to market uncertainty regarding another ECB interest rate hike to reach 4%. Meanwhile, the U.S. Federal Reserve’s (Fed) July rate hike to 5.5% is perceived as its final move before future rate cuts.

In the U.S., both overall and core Consumer Price Index (CPI) stood at 3% and 4.8% in June, with forecasts projecting an increase to 3.3% and 4.8% for July. Despite the upcoming shift in the base effect, which will transition from depressing year-over-year comparisons to elevating them, the monthly increase for July is expected to remain steady at a modest 0.2%. In comparison, the Fed appears to be more advanced in its efforts to combat inflation, while the U.S. economy is displaying greater resilience compared to the euro zone. While the possibility of a soft landing for the U.S. economy is still uncertain, the likelihood of a harder landing for the euro zone seems more plausible.

The EUR/USD currency pair experienced a 0.43% decline, yet found support at 1.0930 lows, coinciding with the 55-day moving average and mirroring last week’s lows. Despite an approximately 8 basis points decline in the two-year bund-Treasury yield spreads, they did not reach their previous lows from August. The adjustment in Treasury yields, in part driven by preparation for a three-day Treasury refunding and influenced by recent auction outcomes, was followed by a subsequent decrease in yields after a strong 3-year auction. The USD/JPY pair saw a 0.57% increase, as the demand for the higher-yielding dollar overpowered the safe-haven appeal of the yen, particularly following certain developments. Furthermore, both the Australian dollar (AUD) and the Chinese yuan (CNH) experienced declines of 0.59% and 0.45% respectively, with USD/CNH surpassing a crucial downtrend line, while concerns about China and global economic growth led to significant losses in industrial metals. The focus is now shifting towards upcoming U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) reports scheduled for Thursday and Friday.

Picks of the Day Analysis

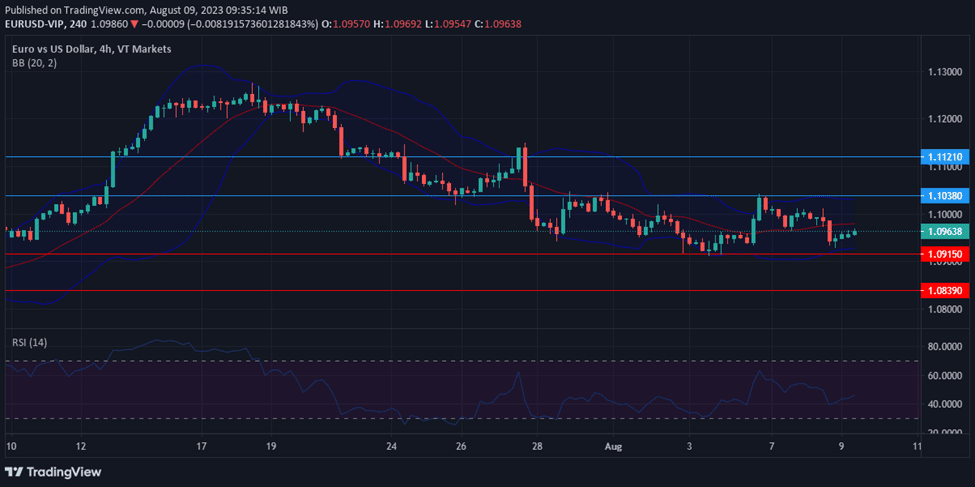

EUR/USD (4 Hours)

EUR/USD Resilient Amid Strong Dollar and Economic Factors

The EUR/USD pair faced losses on Tuesday due to a robust US Dollar and rising risk aversion, yet managed to remain above a vital support level. Italy’s surprise announcement of a bank profits windfall tax caused the Italian stock index to plummet over 2%, while Wall Street indices also dipped following Moody’s downgrade of US banks. The European Central Bank’s June survey indicated decreased inflation expectations, affecting market views on rate hikes. Meanwhile, the US Dollar gained strength amidst risk aversion and mixed messages from Federal Reserve officials. The focus now shifts to Thursday’s influential US Consumer Price Index (CPI) report.

Based on technical analysis, the EUR/USD remained steady on Tuesday as the market awaited upcoming US inflation data for the week, specifically CPI and PPI, while also attempting to move toward the middle band of the Bollinger Bands. Right now, the price is slightly below the middle band, creating a small gap between the upper and lower bands of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 46, showing that the EUR/USD is in a phase of consolidation.

Resistance: 1.1038, 1.1121

Support: 1.0915, 1.0839

XAU/USD (4 Hours)

XAU/USD Hits Four-Week Low as US Dollar Strengthens Amid Fed Remarks and Economic Uncertainty

During the early American trading session, XAU/USD plummeted to a new four-week low at $1,922.74 per troy ounce. This drop was fueled by a surge in demand for the US Dollar following comments from Federal Reserve officials and in anticipation of the upcoming release of the US July Consumer Price Index.

Philadelphia Federal Reserve Bank President Patrick Harker’s statements highlighted a move toward normalcy in economic conditions. Despite optimism for a smooth economic transition, concerns persisted over supply chain issues. Harker also suggested the possibility of the Fed exercising patience with interest rates, depending on future data, including the pivotal decision in September. Despite global stock declines and worries about economic uncertainty, gold’s price decline persisted. However, a slight pullback in Treasury yields prevented a more significant appreciation of the US Dollar.

Based to technical analysis, the XAU/USD experienced a minor decrease on Tuesday, managing to touch the lower band of the Bollinger Bands. Currently, the price is slightly below the middle band within the Bollinger Bands. The Relative Strength Index (RSI) stands at 40, suggesting that the XAU/USD pair is somewhat in a bearish mode.

Resistance: $1,936, $1,954

Support: $1,920, $1,902

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| NZD | Inflation Expectations q/q | 11:00 | 2.5% |