Equities fell on Friday despite a better-than-expected jobs report as a worrying development in Ukraine weighed on the risk sentiment. The Dow Jones Industrial Average declined 0.53% and the S&P 500 dropped 0.79%; the Nasdaq 100 fell the hardest, moving down 1.66% on Friday. Moreover, the US economy notably added 678,000 jobs last month, above the 440,000 expected. The jobs report would be the last one before the Fed’s meeting where it is expected to start raising the interest rates.

The third round of negotiations between Russia and Ukraine will take place early this week. From the last negotiation, both sides have agreed to establish corridors for civilians; despite the agreement, Russia declared that it would press its military action until it completely achieve its goal, the demilitarization of Ukraine.

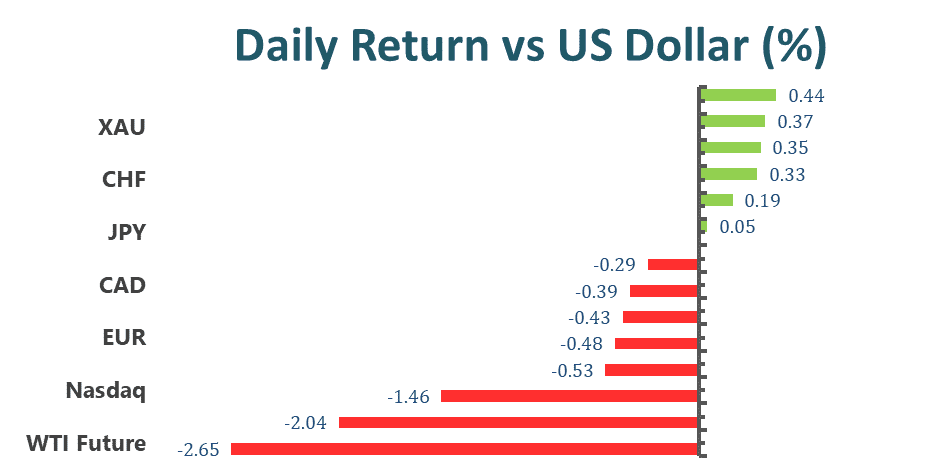

Oil prices are set to continuously surge further due to delays to the conclusion of Iranian nuclear talks and the original topic from Russian supply disruptions. According to Amrita Sen, co-founder of Energy Aspects, oil price could possibly rise to $125, and even to $147.

Main Pairs Movement:

Gold embraced a positive note as the escalation of Russia and Ukraine continues. The tension intensified after Russia’s leader Putin ordered to execute Ukraine’s President Volodymyr Zelensky. Gold closed with $1970.840, the highest level since 2020. Further price action eyes on US inflation report.

WTI rose further toward $114.95 per barrel as Russia supply concerns persisted. Oil prices look to surge further due to the delays in Iranian talks.

EURUSD headed further south, trading at 1.09262 on Friday following the Nonfarm Payrolls that boosted the US dollar towards as high as 98.6320.

The US dollar index continued to head further north following the unbeaten jobs report. With firm economic data and the fundamental crisis in Russia’s invasion of Ukraine, it has boosted the US dollar to a fresh weekly high of 98.6320.

Technical Analysis:

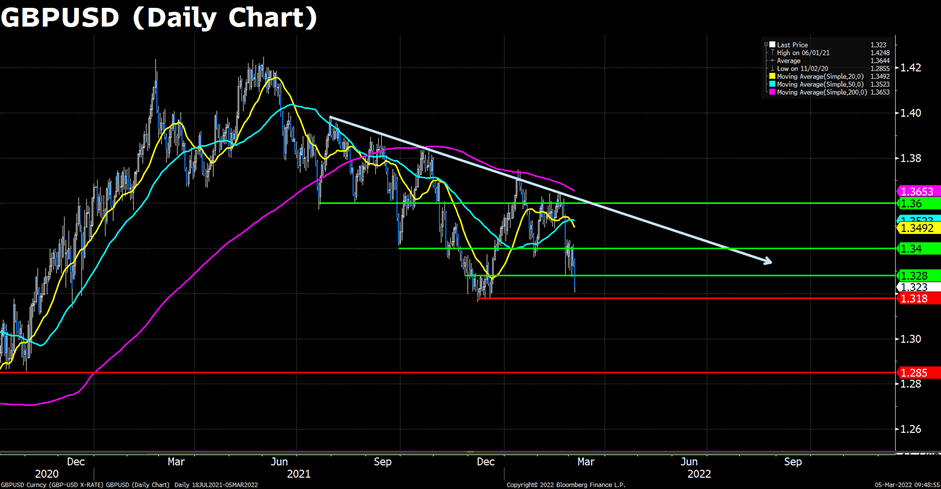

GBPUSD (Daily Chart)

Cable continued its downside traction in a busy Nonfarm Payrolls week, plummeting to the lowest level in three months below mid-1.3200s. Risk-off sentiments are still the main topic in the recent market, as the Russian invasion in Ukraine failed to subside despite two rounds of ‘peace talks’. Emerging stagflation risks amid soaring commodity prices will likely keep Sterlings unattractive in a relatively light week ahead, as investors remain on edge due to the ongoing Ukraine crisis.

On the technical front, the cable is still capped by the mid-to-long term downtrend from August 2021. The pair at the moment traded below all its major moving averages (20,50 and 200 SMA), and both the RSI indicator and MACD histogram show strongly bearish sentiments for the pair. On the downside, the immediate support for the pair locates at 1.3180. On the flip side, the major resistance will appear at 1.3280 in cases the pair rebounded.

Resistance: 1.3280, 1.3400, 1.360

Support: 1.3180, 1.2850

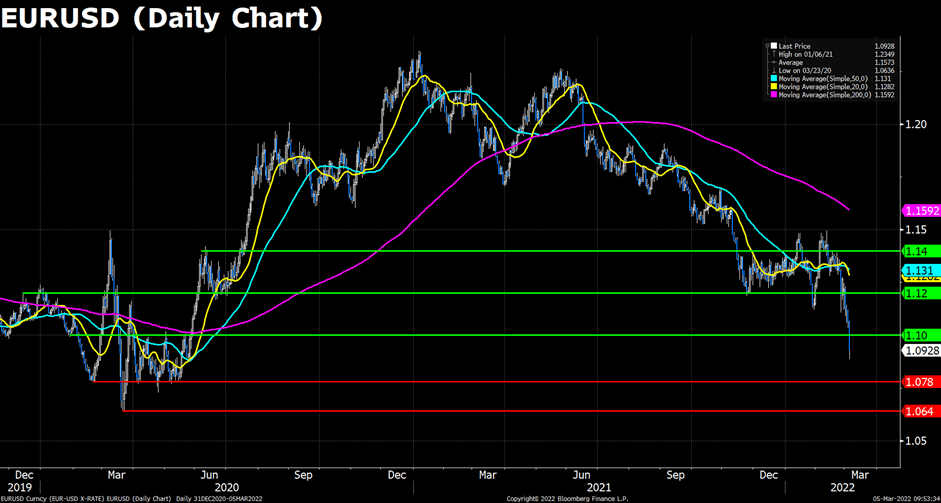

EURUSD (4-Hour Chart)

Euro price has hit a low of 1.0885 – a level not seen since May 2020. Much of the shared currency’s losses can be attributed to the ongoing war at its borders. The Russian war against Ukraine is now moving to the ninth day. Regardless of two rounds of peace talks, Moscow has shelled Europe’s largest nuclear plant, Zaporizhzhia, on Friday. An explosion there could be as much as ten times worse than that in Chernobyl.

As to technical, the euro pair has been in free fall since February. The long-term bearish trend was breached twice this year, but unfortunately, a series of bad news capped the upside momentum and dragged the pair back down below the 1.1000 price level. On the downside, the pair’s last barricade to a thorough collapse sits at 1.0780, and any attempts to recovery will have to challenge the psychological resistance at 1.1000.

Resistance: 1.1000, 1.1200, 1.1400

Support: 1.0780, 1.0640

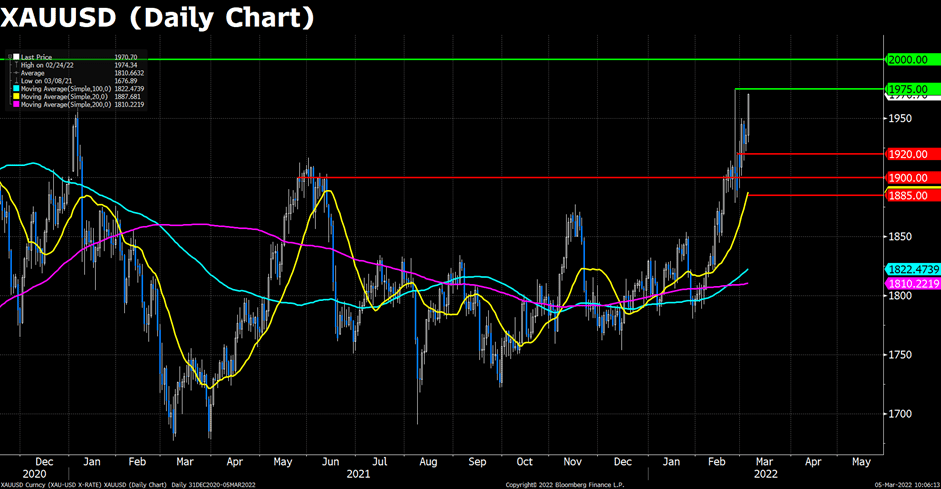

XAUUSD (4-Hour Chart)

Gold continues to find demand amid the ongoing Russia-Ukraine crisis. On Wednesday, the US Bureau of Labor Statistics will release the February Consumer Price Index (CPI) data. Unless there is a negative surprise, investors should continue to price in a hawkish Fed policy outlook. Another leg higher in the US T-bond yields on a strong CPI print could limit the yellow metal’s gains.

The technical picture suggests that XAU/USD remains bullish in the near term, pointing to additional gains towards $1,975. On the upside, $1,975 (February 24 high) aligns as the first hurdle before the precious metal could target the crucial $2,000 level. As long as $1,920 support holds, sellers are likely to remain on the sidelines. Below $1,920, next support is located at $1,900 (psychological level) before $1,885 (20-day SMA).