Healthcare stocks usually offer stability during uncertain times, but something unusual happened this past year. The sector dropped by 29%, marking its worst performance among all S&P 500 sectors. This unexpected decline has traders wondering: what went wrong, and does this dip offer an opportunity?

Usually, healthcare companies thrive even when the economy struggles. People still need medications, medical devices, and hospital visits no matter what. As the global population ages and chronic illnesses become more common, demand for these services remains strong.

Despite these solid long-term prospects, healthcare companies faced unexpected pressures over the past twelve months.

A key reason for the downturn is rising costs, especially in big healthcare firms like UnitedHealth Group (UNH). After the pandemic, more people—particularly older demographics—visited healthcare providers than companies anticipated. This higher usage drove medical costs upwards, squeezing profit margins significantly. Traders became even more cautious after UnitedHealth’s CEO resigned, followed by the company pulling back on its earnings forecasts for the year.

Yet UnitedHealth continues to show solid growth. Its revenue steadily climbed past $400 billion in 2023, though rising costs prevented profits from keeping pace. Looking ahead, the company plans to adjust premium pricing and manage costs more efficiently, aiming to improve profitability.

UnitedHealth’s financial position is also solid, with strong cash flow supporting dividends and operations, although traders should keep an eye on rising debt levels, which reached $76.9 billion, substantially higher than a decade ago. While debt-funded growth makes strategic sense, careful management remains crucial.

For traders, UnitedHealth stock currently looks undervalued. The stock’s intrinsic value is estimated at about $570 per share, making its forward price-to-earnings ratio of 13.2 appear attractive. If UnitedHealth can control costs effectively, its shares may rebound once short-term headwinds ease.

Another standout healthcare company, Novo Nordisk, offers a slightly different story. The Danish pharmaceutical giant saw rapid revenue growth thanks to its blockbuster diabetes and weight-loss treatments. Profit margins reached an impressive 48%, much higher than most healthcare companies.

However, Novo Nordisk faces different risks, particularly related to high market expectations and dependence on successful drug approvals. Increased competition from companies like Eli Lilly could also impact its future performance.

In 2023, Novo Nordisk significantly increased its debt, surpassing $14 billion after acquiring three Catalent manufacturing sites. The move strategically boosted manufacturing capabilities but increased financial risks. Still, Novo’s cash flow remains strong enough to comfortably handle dividends and growth investments.

Importantly, its Return on Invested Capital (ROIC) consistently beats its cost of capital, indicating efficient management. With analysts estimating an intrinsic value around $150 per share, far above its current trading price near $80, Novo Nordisk also looks undervalued, despite a slightly higher forward P/E of 19.5, justified by stronger growth prospects.

Given current global conditions, healthcare stocks might soon attract more attention again. Continued concerns around tariffs, persistent inflation, and slowing global economic growth might encourage traders to reconsider healthcare’s defensive qualities.

Despite recent challenges, the healthcare sector’s underlying demand remains strong, suggesting the current downturn could represent a cautious buying opportunity.

Traders should carefully watch company-specific risks, such as UnitedHealth’s debt and Novo Nordisk’s regulatory sensitivities. But with valuations looking appealing and long-term fundamentals intact, healthcare stocks could gradually regain trader confidence in the months ahead.

Price Movements of the Week

With the broader healthcare sector navigating turbulent waters, traders should remain attentive to specific price zones and critical support and resistance levels across major currencies, commodities, and indices. Understanding these technical price movements can help investors make informed decisions as market conditions evolve throughout the coming week.

The US Dollar Index (USDX) recently climbed from the 98.20 area, though buyers appear hesitant. With this weakness, we could see the index trade slightly lower before any renewed upward momentum emerges. Watch closely for bullish price signals around the 97.70 zone. If buying strength resumes, the next critical zone to watch is around 99.00.

The Euro against the US Dollar (EURUSD) broke above 1.15297, suggesting potential upside movement. However, traders should remain cautious near 1.1550, where bearish activity could emerge. Should prices retreat, focus attention on the support level at approximately 1.1420.

The British Pound versus US Dollar (GBPUSD) encountered firm resistance near the 1.3510 zone. Traders should closely monitor for bearish signals around 1.3485, particularly if the market consolidates at current levels. In the event of further upward pressure, 1.3560 would become another critical resistance area. Conversely, downside movements will test supports around 1.3360 and possibly 1.3315.

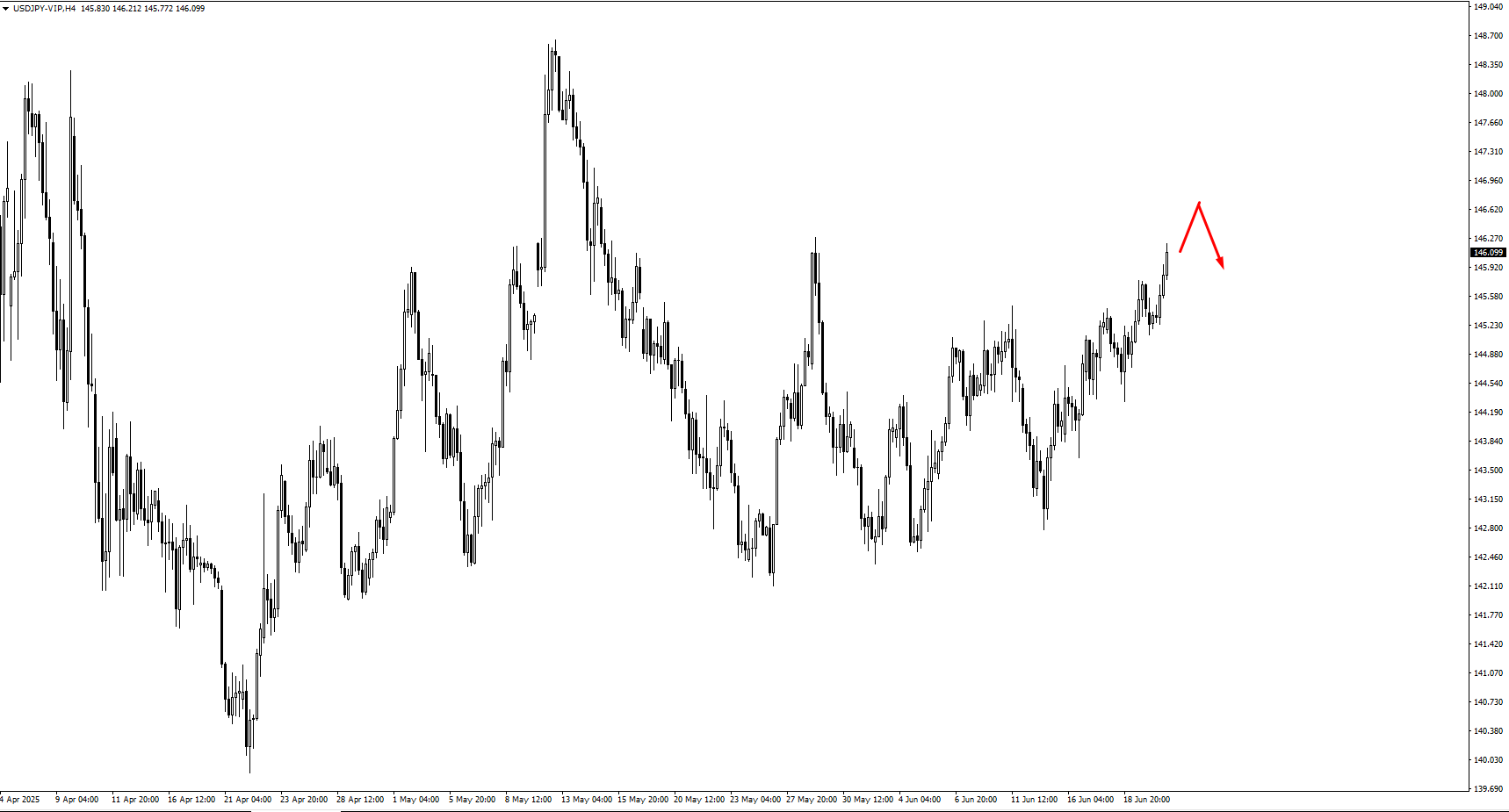

The US Dollar against the Japanese Yen (USDJPY) continues to push higher after temporarily pausing near the 145.75 resistance zone. Traders should prepare for bearish pressure around 146.55 and closely monitor price actions in subsequent sessions.

The US Dollar against the Swiss Franc (USDCHF) currently sees limited selling activity around 0.8220. Prices could edge higher, targeting the 0.8200 level, but any new upward swing would likely invite fresh bearish activity at the 0.8220 level once again.

The Australian Dollar against the US Dollar (AUDUSD) faces stiff resistance at the closely monitored 0.6500 zone. A critical test will be the upcoming encounter with its underlying trendline. Traders should be ready for decisive price action once this occurs.

The New Zealand Dollar against the US Dollar (NZDUSD) has recently declined from the 0.6025 resistance area. Further downside pressure could test levels around 0.5940 or even down to 0.5900, presenting critical zones to watch for potential reactions.

For the US Dollar against the Canadian Dollar (USDCAD), the 1.3715 area provided only minor resistance, suggesting upward momentum remains possible. Traders should carefully observe price actions approaching the next critical zone at 1.3795.

In commodities, US Oil is poised for further volatility, driven by geopolitical events such as recent US actions towards Iran. As oil prices continue upwards, the next important resistance area to monitor is around 83.90.

Gold has found solid footing at the 3330 support zone, with potential for upside momentum. Should prices rise further, the 3410 level becomes crucial to watch for market reactions.

Turning to indices, the S&P 500 faces downward pressures amid geopolitical uncertainties. Traders should closely watch for price actions around the key support area at 5810.

In cryptocurrency markets, Bitcoin (BTC) declined sharply from the 106825 area, subsequently breaking below the 103358 support. The ongoing geopolitical tensions involving the US and Iran could intensify pressure on Bitcoin. If the critical low at 100396 breaks, traders should anticipate deeper consolidation or further downward moves.

Lastly, Natural Gas prices sharply retreated after nearing the resistance at 4.06. Further consolidation at current levels could push prices toward a lower critical support zone at 3.57. Traders should watch for clear signals at this level for directional guidance.

Key Events of the Week

The trading week kicks off with important PMI data from Europe, the UK, and the US, setting the tone for currency markets.

On Monday, June 23, Europe’s economic health comes into focus. German Flash Manufacturing PMI is forecasted slightly higher at 48.9, up from a previous 48.3, while Services PMI is expected at 47.8 compared to the previous 47.1. With these improved outlooks, the EUR may find early-week support.

In the UK, Flash Manufacturing PMI should inch upward to 46.9 from 46.4, and Services PMI is anticipated to rise modestly to 51.2 from 50.9. This improvement in business activity could boost the GBP in the early sessions.

Across the Atlantic, US PMI figures suggest potential softness. Flash Manufacturing PMI is projected to drop slightly to 51.1 from 52.0, while Services PMI might decline to 52.9 from 53.7. Consequently, traders might see downward pressure on the USDX earlier in the week.

Moving onto Tuesday, June 24, Canada’s inflation data (CPI m/m) will be closely monitored, with an expected rise of 0.5% from the previous month’s -0.1%. This spike could initially push USDCAD higher, but a pullback might soon follow.

On Wednesday, June 25, Australia releases annual CPI data, with forecasts stable at 2.4%. Traders should carefully consider price structure around this release for clearer signals.

By Thursday, June 26, the US Final GDP quarterly data will be reported, holding steady expectations at -0.2%. This unchanged forecast prompts traders to focus closely on market structure and price patterns rather than expecting major volatility from this data alone.

Lastly, Friday, June 27, brings the US Core PCE Price Index monthly figures, expected unchanged at 0.1%. Like previous events, market participants should reference existing technical structures and cautiously gauge market reactions accordingly.

Overall, these economic updates provide crucial insights, helping traders navigate currency and equity markets with informed caution this week.