Overview

This week’s spotlight is on major central banks. The Federal Reserve, Bank of Japan, and European Central Bank, with traders bracing for policy signals that could define the market’s next big move.

The US dollar index (USDX) has cooled near 98.80 after retreating from 99.28, while gold steadies around USD 4,190 after a brief pullback.

All eyes are now on how upcoming rate decisions and inflation data will shape global sentiment.

If the Fed confirms a 25–50 bps rate cut and the BOJ hints at a December lift-off, markets could see sharp cross-asset rotation. Meanwhile, mega-cap earnings from Apple, Microsoft, Alphabet, Meta, and Amazon could drive short-term swings in US equities.

Central Banks in Focus

Federal Reserve: Approaching the Pivot Point

Traders largely expect a 25 bps Fed rate cut this week, with some still pricing the chance of a deeper 50 bps move. Key data, Advance GDP (forecast 3.0% q/q vs. 3.8% prior) and Core PCE (expected 0.2% m/m), will be critical in confirming whether the Fed’s easing stance remains justified.

A dovish Fed could weaken the dollar further, boosting gold and risk assets, but traders are likely to remain cautious until Chair Powell’s statement provides clarity on how far and fast easing could go.

Bank of Japan: Eyes on a December Hike

Japan’s inflation remains above target, with core CPI at 2.9% y/y and services PMI at 52.4, indicating steady domestic demand. However, manufacturing PMI slipped to 48.3, suggesting underlying fragility.

Markets expect a “hawkish hold” at this week’s meeting, keeping the door open for a potential rate hike to 0.75% in December.

If the Fed cuts while the BOJ tightens later, it could narrow the USDJPY yield gap, pulling the pair lower into year-end.

Key Instruments to Watch

XAUUSD (Gold) | USDJPY | SP500 | USOIL | USDX

Upcoming Events

| 27 Oct | AUD | RBA Gov Bullock Speaks | — | — | Tone may reveal bias amid inflation pressures. |

| 29 Oct | AUD | CPI y/y | 3.10% | 3.00% | A stronger print could fuel AUD strength ahead of Nov meeting. |

| 29 Oct | CAD | Overnight Rate | 2.25% | 2.50% | BoC expected to pause; focus on policy outlook. |

| 30 Oct | USD | Federal Funds Rate | 4.00% | 4.25% | A 25–50 bps cut likely; market reaction hinges on Powell’s tone. |

| 30 Oct | JPY | BOJ Policy Rate | 0.50% | 0.50% | Hawkish hold expected; watch for December hike hints. |

| 30 Oct | USD | Advance GDP q/q | 3.00% | 3.80% | Slowing growth could reinforce dovish bias. |

| 30 Oct | EUR | Main Refinancing Rate | 2.15% | 2.15% | ECB likely on hold; inflation commentary in focus. |

| 31 Oct | USD | Core PCE Price Index m/m | 0.20% | 0.20% | Key gauge for Fed’s future trajectory. |

Market Movements to Watch

Gold (XAUUSD)

Gold eased from USD 4,190 resistance.

A break above USD 4,200 could target USD 4,275, while USD 4,000 remains the key support.

Watch PCE data for directional cues.

US Dollar Index (USDX)

Currently near 98.80, with resistance around 99.28–99.80.

A dovish Fed could drag the index below 98.50, while a mild cut could stabilize it above 99.00.

USDJPY

Trading above 153.20.

A hawkish BOJ could send it toward 151.80, while steady policy might keep resistance near 153.80–154.00.

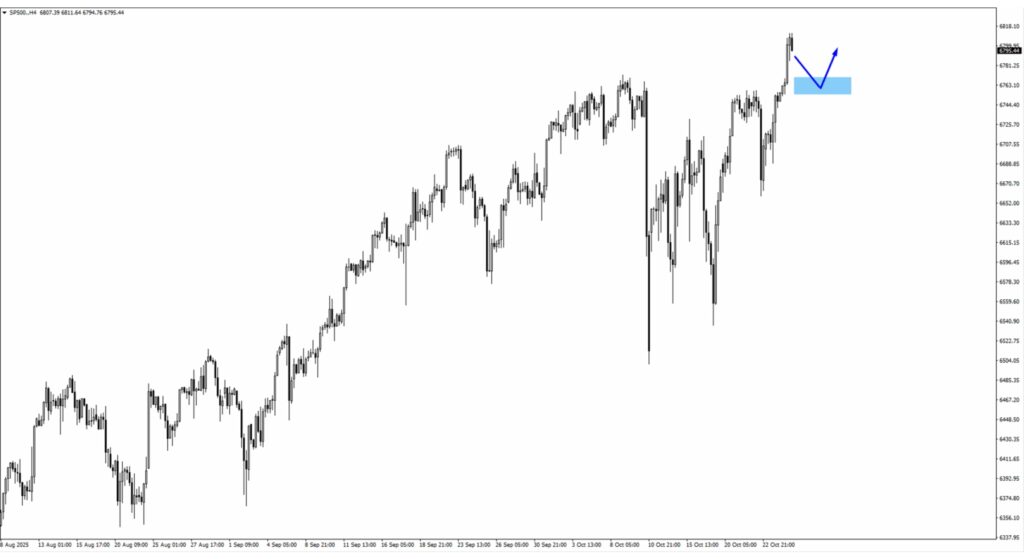

SP500

Testing new highs, with support at 6,750.

Big-tech earnings will steer momentum.

A sustained move above 6,800 keeps the uptrend alive.

USOil

Consolidating near USD 61.00–60.30 support.

A breakout above USD 62.50 may target USD 65.00.

Demand outlook remains tied to global growth signals.

Bottom Line

Markets are entering a pivotal week led by Fed and BOJ decisions that could redefine global rate dynamics.

Expect volatility across gold, yen, and US indices as traders reposition for the next macro shift.

With central bank updates and major earnings converging, staying agile could be the key to capturing the next big opportunity.