Key Points

- December rate-cut expectations have surged to nearly 87%, but the outlook remains data-dependent as ISM PMI, ADP employment, and the PCE price index serve as the final major signals before the FOMC.

- This week’s economic releases could either support or reverse the rapid dovish repricing.

- Additional volatility may come from BoJ Governor Ueda’s speech, Australian GDP, and Canada’s labor market report.

The swift shift in market expectations followed rare dovish remarks from typically centrist Fed members, including New York Fed President John Williams and Governor Christopher Waller. Their comments suggested that rate cuts may be needed “in the near term” as inflation cools and labor conditions soften, prompting institutions like JPMorgan to advance their forecast for an initial rate cut to December.

Growing Expectations of a Cut

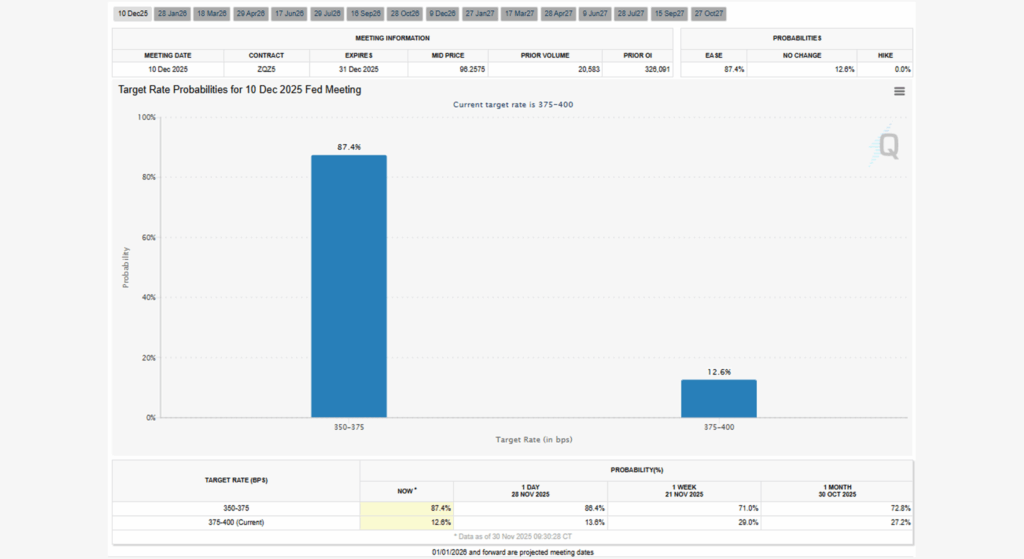

FedWatch probabilities have moved sharply over the past two weeks. Futures now reflect an 87% likelihood of a 25 bp cut at the 10 December FOMC meeting, compared with roughly 40–50% just days earlier.

The shift has filtered directly into the bond market:

- The 10-year Treasury yield has eased toward 4.0%.

- The 2-year yield is around 3.5%, in line with expectations of multiple cuts in 2026.

Lower yields have reignited the appetite for growth assets. US tech stocks recorded their biggest rally in six months, with Nasdaq up 2.7% and the S&P 500 up 1.6%, driven by strong performances from AI-linked names such as Broadcom, Alphabet, Microsoft, and Tesla.

Crypto, however, remains near November lows, reflecting lingering caution despite improved liquidity expectations. Volatility remains elevated ahead of the US data releases.

Key Symbols to Watch

USDX | XAUUSD | USDCAD | AUDUSD | BTCUSD

Upcoming Events

| 1 Dec | USD | ISM Manufacturing PMI | 49.0 | 48.7 | Watch for USD volatility |

| 3 Dec | AUD | GDP q/q | 0.7% | 0.6% | Weak GDP may pressure AUD |

| 3 Dec | USD | ADP Non-Farm Employment | 19K | 42K | Major swing factor for USD |

| 3 Dec | USD | ISM Services PMI | 52.0 | 52.4 | Softer data boosts risk sentiment |

| 4 Dec | USD | Unemployment Claims | 220K | 216K | Rising claims reinforce dovish bias |

| 5 Dec | CAD | Unemployment Rate | 7.0% | 6.9% | Strong jobs could lift CAD |

| 5 Dec | USD | Core PCE m/m | 0.20% | 0.20% | Soft PCE may support gold |

Key Movements of the Week

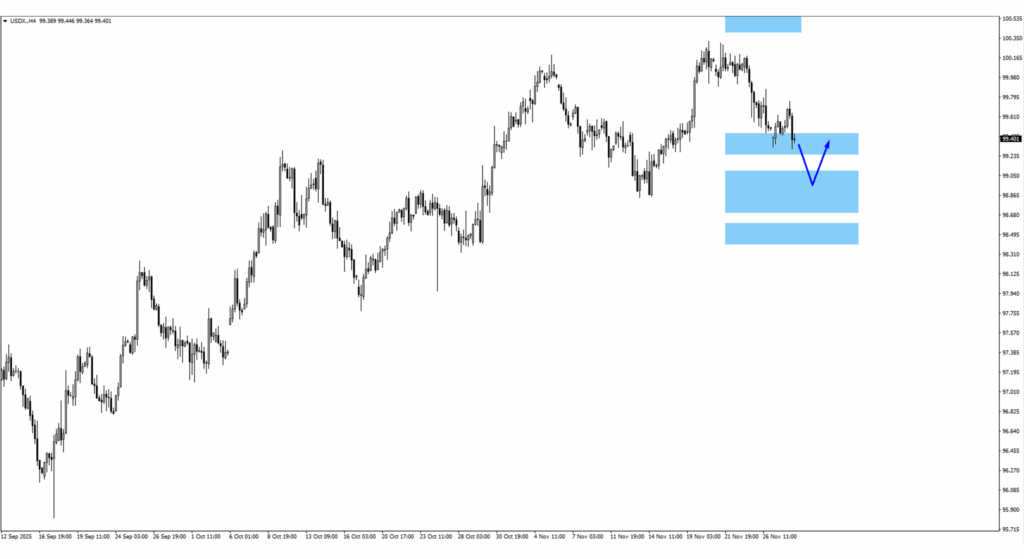

USD Index (USDX)

USDX retested the 99.45 zone, showing hesitation as markets digest shifting rate expectations.

- A pullback toward 99.00 may attract bullish reactions.

- Strong data could drive a push toward 100.50–100.90.

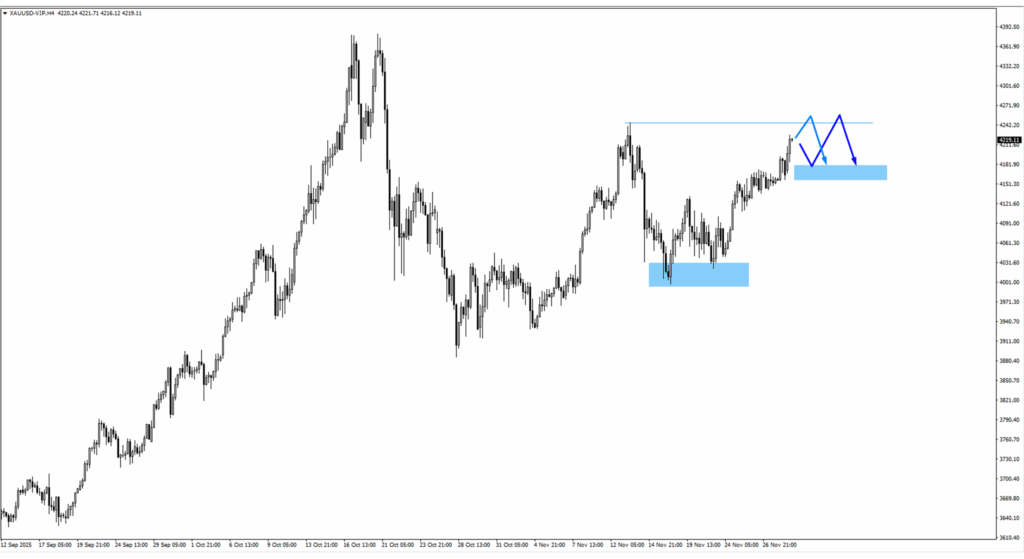

Gold (XAUUSD)

Gold remained above the 4,190 monitored area, supported by lower yields and rising expectations of a December cut.

- Upside targets: 4,245 resistance.

- Watch 4,170 for bullish reactions if US data softens.

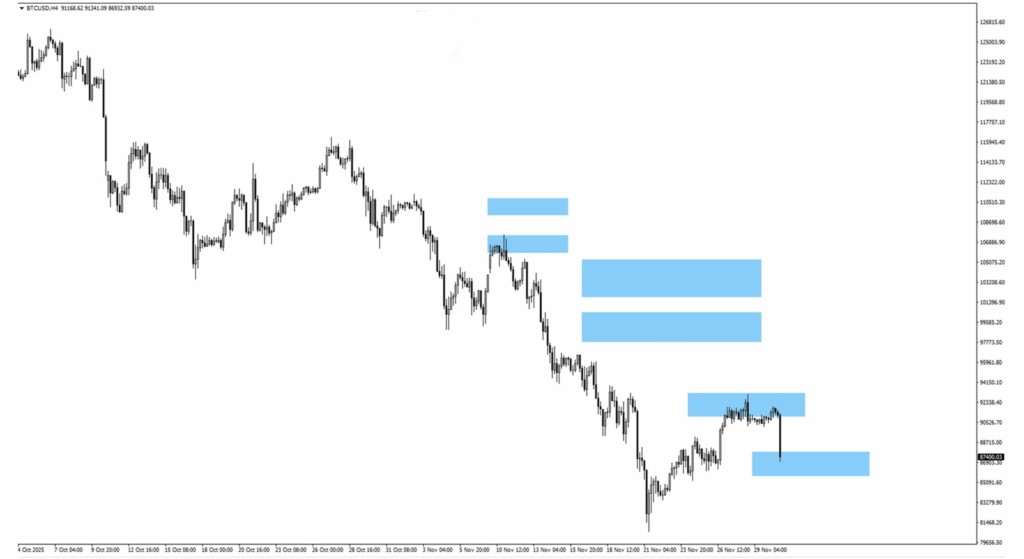

Bitcoin (BTCUSD)

BTC slipped from 92,450 after a week-long consolidation and is testing the 87,070 level as traders await US data.

- Another consolidation may lead to a fresh swing low if data strengthens the USD and tempers cut expectations.

USDCAD

USDCAD continued lower after clearing the 1.3970 liquidity zone.

- Next support: 1.3900.

- Canada’s jobs report on 5 December will be pivotal for direction.

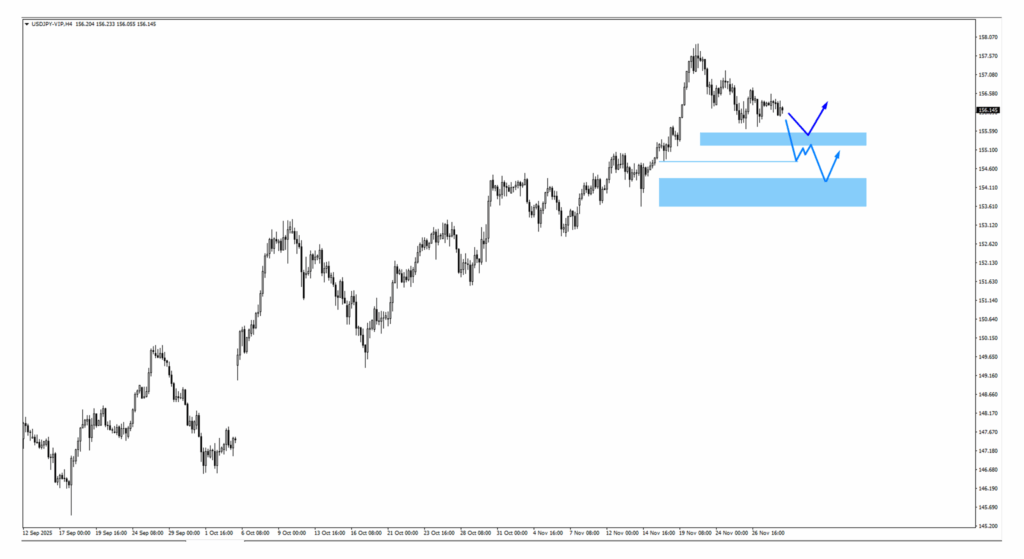

USDJPY

USDJPY extended its decline to 155.50 following BoJ Governor Ueda’s signal that a December rate hike remains possible.

- Key levels to monitor: 155.35 and 154.65, though strong BoJ messaging may keep the pair pressured.

Bottom Line

This week’s US data will determine whether the dovish shift can deepen or needs moderation. With influential updates from Japan, Australia, and Canada also in play, cross-asset volatility is likely to remain elevated.

Traders should stay agile, monitor key levels closely, and be prepared for abrupt moves as markets position for the final major event of the year.