The week ahead appears light on the economic calendar but active on the charts. As year-end liquidity thins, even modest data surprises could push USD, gold, and crypto beyond their recent ranges.

The Bank of Japan raised its policy rate to 0.75% on 19 December, the highest level in three decades, confirming a gradual exit from ultra-loose monetary policy.

Markets had feared a sharp unwind of the yen carry trade, yet the initial reaction remained orderly.

US equity futures firmed, and Bitcoin rallied following the decision, signalling that the hike was largely priced in. Governor Ueda reinforced this calm by emphasizing that policy remains below the estimated neutral rate.

Real yields in Japan remain negative, maintaining accommodative financial conditions.

For traders, this is important, as the yen still lacks sufficient yield appeal to trigger forced deleveraging across global assets. Any carry-trade unwind is more likely to unfold over several months rather than a few days.

US Growth Signals Take Centre Stage

Attention now shifts to the US preliminary GDP for Q3, forecast at 3.2% versus the previous 3.8%. A softer print would reinforce expectations that US growth peaked earlier in the year.

The dollar index rebounded from the 97.40 zone last week, but upside momentum appears fragile. If GDP confirms slowing growth, USD strength could fade again, supporting commodities and risk assets into year-end.

Liquidity conditions also thin rapidly this week, which often amplifies technical moves around key levels.

Risk Assets Hold Their Nerve

Equities and crypto continue to digest the idea that global tightening is becoming more predictable. The absence of policy shocks has kept risk appetite intact, though follow-through depends on whether growth data weakens further.

Bitcoin remains range-bound, reflecting balance rather than conviction. Gold continues to attract dip-buying interest as real yield expectations remain capped.

Key Symbols to Watch

USDX | USDJPY | XAUUSD | BTCUSD | SP500

Upcoming Events

| 23 Dec | USD | Preliminary GDP q/q (Q3) | 3.20% | 3.80% | A softer growth print may cap USD upside and support commodities and risk assets |

Key Movements of the Week

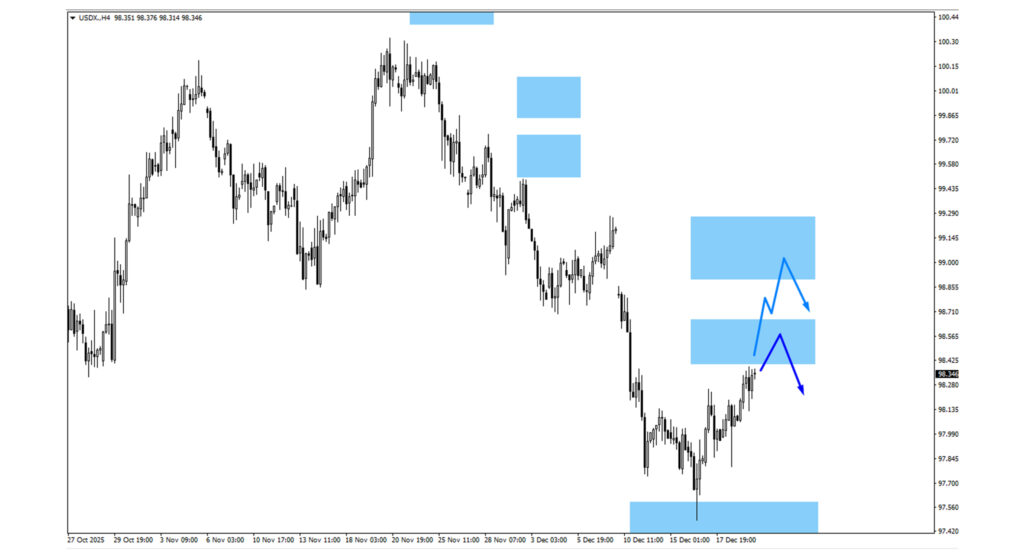

US Dollar Index (USDX)

- USDX rebounded from the 97.40 monitored zone last week.

- Resistance sits near 98.55, with scope toward 99.10 if momentum holds.

- A weak GDP print could reverse gains back into range.

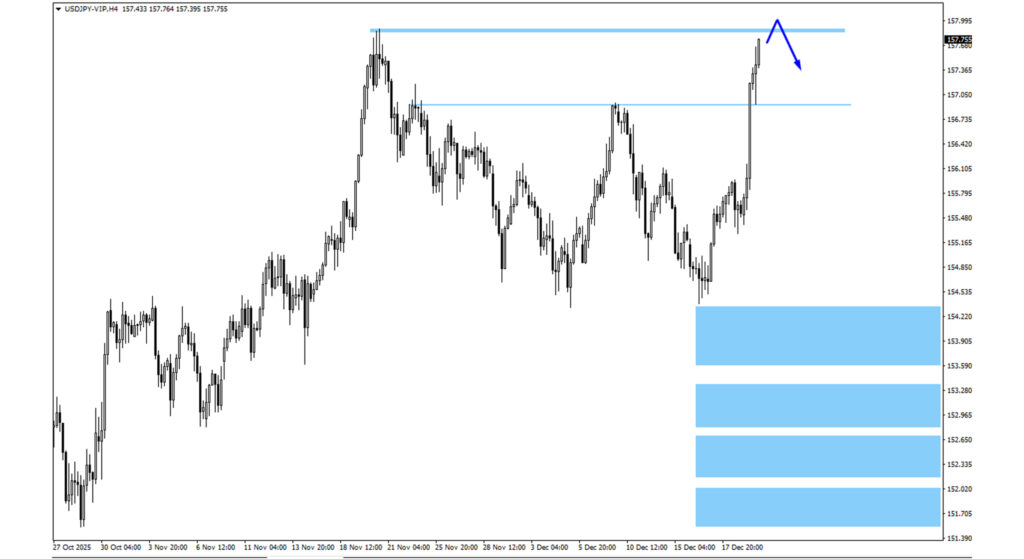

USDJPY

- USDJPY pushed higher following the BOJ decision.

- Price may test above 157.88 before encountering selling pressure.

- Failure to hold above recent highs may signal consolidation rather than a trend.

Gold Price (XAUUSD)

- Gold bounced from the 4,290 zone but lacks strong continuation.

- Pullbacks toward 4,290 or 4,215 may attract dip buyers.

- Direction depends on US data and the USD reaction.

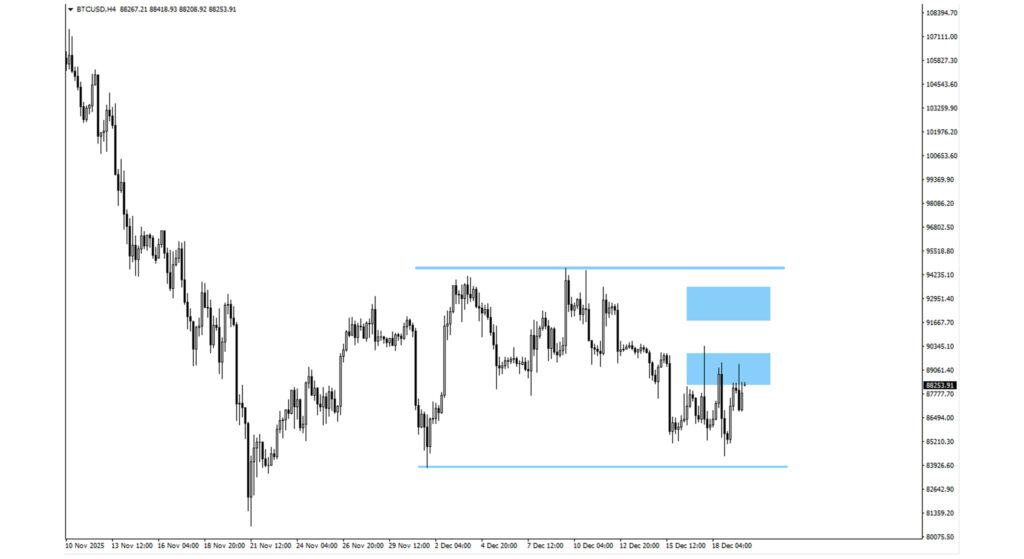

Bitcoin (BTCUSD)

- Bitcoin remains range-bound near 89,250.

- A close below 83,814 opens the downside toward 75,850.

- A break higher shifts focus to 91,780 resistance.

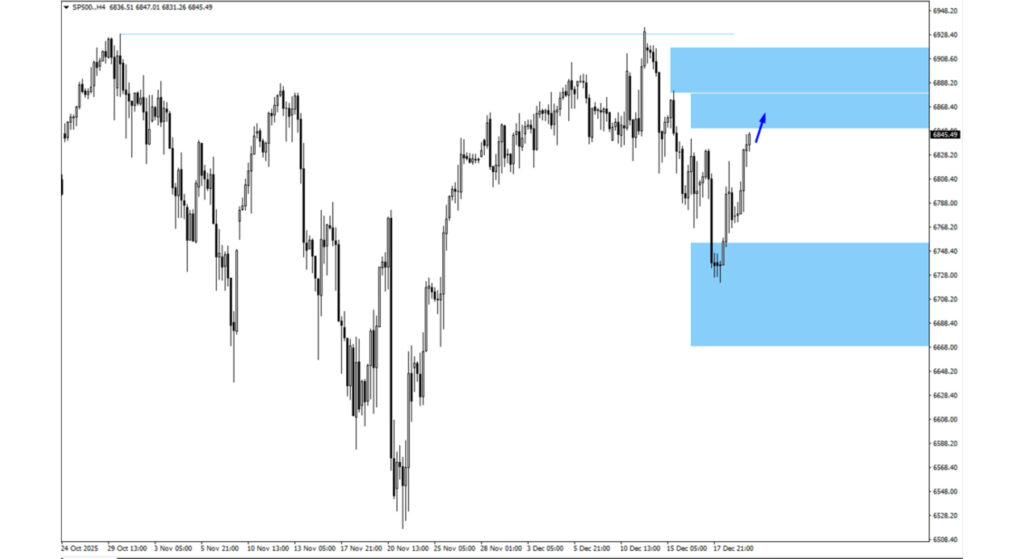

S&P 500 (SP500)

- The index rebounded strongly from recent lows.

- Upside levels to monitor sit near 6,870 and 6,905.

- Holiday liquidity may exaggerate intraday moves.

Bottom Line

Markets enter the week in a transition phase, shifting from policy-driven volatility toward technically led trading. Japan’s move away from ultra-loose policy has so far avoided disruption, allowing risk sentiment to remain stable as traders reassess positioning.

Focus now turns to US growth data and the dollar’s response. A softer GDP outcome may limit USD upside and support commodities and risk assets, while thin holiday liquidity raises the risk of exaggerated moves around key levels.