Market Focus

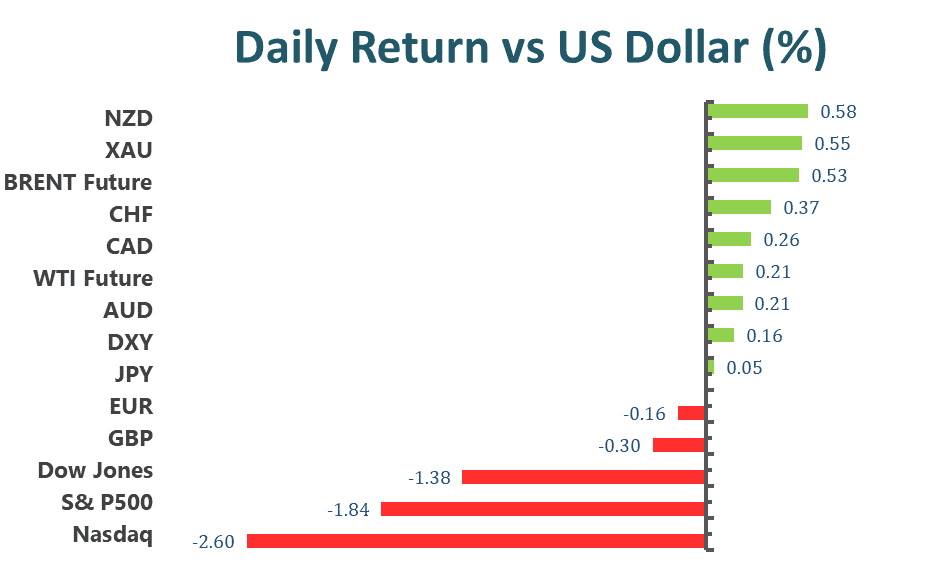

Wall street three major indexes ended sharply lower on Wednesday, extending recent losses as Ukraine declared a state of emergency and the U.S. State Department said the possibility of a Russian invasion of Ukraine remained looming. Hence, as tensions escalate, the Dow is also facing a correction. Despite rising tensions and no sign the Russians will back down, the White House said President Joe Biden has no intention of sending U.S. troops to fight in Ukraine. However, the United States has taken some action, imposing further sanctions on Nord Stream 2 AG, the company responsible for the construction of Russia’s Nord Stream 2 gas pipeline, aimed at limiting Russia’s ability to raise money from the West. Meanwhile, the European Union is scheduled to hold an emergency summit on Thursday to discuss Russia’s next steps after its entry into Ukraine. At the end of the market, the Dow Jones Industrial Average fell 1.38% to 33,131.76 points, the S&P 500 index lost 1.84% to 4,225.50 and the Nasdaq Composite Index dropped 2.57% to 13,037.49 points.

10 sectors in the S&P 500 ended lower, with the consumer discretionary falling the most, down 3.42%, followed by technology and industrials sectors, down 2.56% and 1.88%, respectively. The lone winner was the oil-related sector, energy, which rose 1.01%. Geopolitical tensions aside, a string of quarterly earnings from consumer discretionary companies including TJX Companies, Lowe’s Companies and Caesars Entertainment was in focus. TJX Corporation fell 5% after reporting fourth-quarter results, as higher costs and supply chain disruptions caused by the pandemic weighed on growth. Meanwhile, Lowe’s pared some of its gains as strong demand for home improvement tools and building materials boosted fourth-quarter results, but rose about 1% after issuing better-than-expected guidance. Caesars Entertainment reported a narrower quarterly loss as demand rebounded and revenue surged after pandemic restrictions eased. Its shares rose more than 3%.

Main Pairs Movement:

Investors were upbeat about developments in Eastern Europe on the day, but sentiment soured during U.S. trading hours, sending the greenback stronger against most of its major rivals. Ukraine has declared a state of emergency for 30 days starting on February 24, and U.S. intelligence reports have suggested that Russia could invade within the next 48 hours despite multiple Western sanctions on Russia. Additionally, several Ukrainian government websites went offline after blaming Russia for the DDoS attack.

EUR/USD remained in a consolidating range around 1.1300, slowly heading south to hit weekly lows.

GBP/USD also weakened below 1.35800 and returned to consolidation area. On the other hand, commodity-linked currencies were lower, but maintained their intraday gains. AUD/USD rose for a third day, hitting a daily high of 0.72838, but then pared gains to settle near 0.7230.

The safe-haven Swiss franc and Japanese yen edged higher against the dollar, with gold continuing its gains and holding above the 1900 level.

On the other hand, oil prices closed higher again, with WTI up 0.73% and Brent up 0.66%.

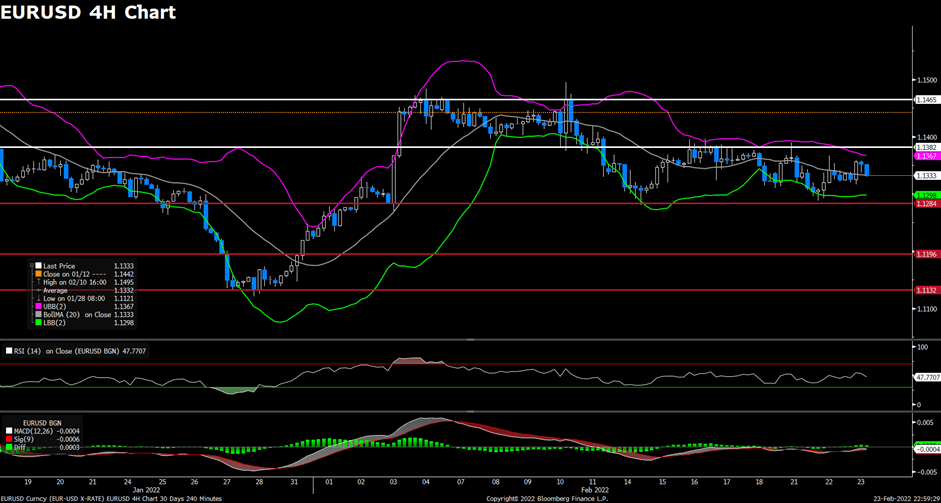

EURUSD (4-Hour Chart)

The EUR/USD pair edged higher on Wednesday, extending its previous rally from a weekly low that touched yesterday amid risk-on market environment. The pair preserved its bearish momentum and touched a daily low in early European session, but then started to rebound back to 1.1350 area to erase all of its daily losses. The pair is now trading at 1.1333, posting a 0.08% gain on a daily basis. EUR/USD stays in the positive territory amid weaker US dollar across the board, as the upbeat market mood make it difficult for the greenback to find demand. However, the US and several European leaders both announced sanctions against Russia, therefore developments in Eastern Europe might limit the losses for the greenback. For the Euro, hawkish comments by ECB’s Board member R.Holtzmann has lent support to the EUR/USD pair, as he said that it’s possible for ECB to hike rates before ending bond purchases.

For technical aspect, RSI indicator 47 figures as of writing, suggesting that bear is preserving strength as the RSI is moving south. As for the Bollinger Bands, the price retreated back to the moving average, which indicates that the downside traction could persist. In conclusion, we think market will be slightly bearish as long as the 1.1382 resistance line holds. Tensions between Russia and Ukraine will remain to be market focus.

Resistance: 1.1382, 1.1465

Support: 1.1284, 1.1196, 1.1132

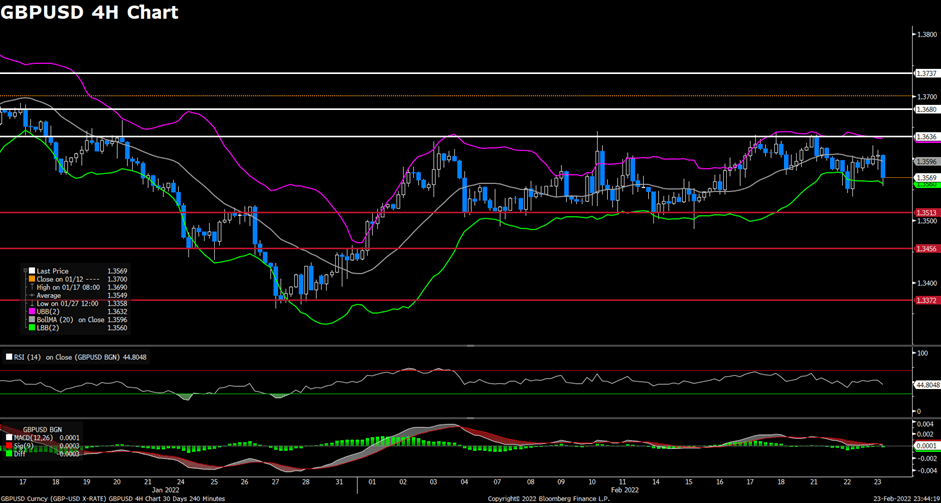

GBPUSD (4-Hour Chart)

The pair GBP/USD declined on Wednesday, lacking further strength to extend the rally from one-week lows amid dovish BoE comments. The pair was flirting with 1.3580~1.360 area during Asian session, then started to see some selling and dropped towards 1.3570 level heading into American session. At the time of writing, the cable stays in negative territory with a 0.06% loss for the day, remaining under pressure on recovering US dollar. The sanctions announced by the US against Russia were not as harsh as feared by the market, weighing on safe haven assets and favored investors’ sentiment. For British pound, Bank of England Governor Andrew Bailey said that they have two-sided risks to their inflation forecasts and higher interest rates will also raise unemployment and slow growth. Therefore, the hawkish comment acted as a headwind for the cable and capped its upside.

For technical aspect, RSI indicator 43 figures as of writing, suggesting that downside is more favored as the RSI stays below the mid-line. For the Bollinger Bands, the price is moving out of the lower band, indicating a strong trend continuation. In conclusion, we think market will be slightly bearish as the pair failed to test the 1.3636 resistance, but the cable need a break below 1.3513 support to open the road for additional losses.

Resistance: 1.3636, 1.3680, 1.3737

Support: 1.3513, 1.3456, 1.3372

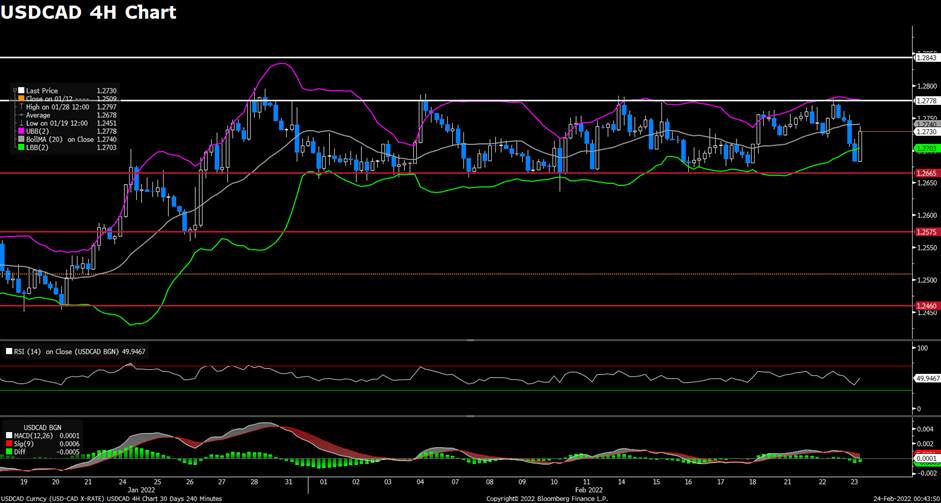

USDCAD (4-Hour Chart)

As the risk-on mood weighed on the safe-haven US dollar today, the pair USD/CAD came under bearish momentum and extended its slide from 1.2780 area. The pair suffered heavy losses most of the day and dropped to a weekly low below 1.2690 level, now bouncing back slightly to recover some of its daily losses. USD/CAD is trading at 1.2730 at the time of writing, losing 0.32% on a daily basis. The new economic sanctions on Russia were not as bad as market’s expectation, easing the concerns about Russia/Ukraine conflict and disfavored the safe-haven greenback. On top of that, surging crude oil prices also lend strong support to the commodity-linked loonie and undermined USD/CAD pair. WTI now bounces back to the $92.00 per barrel area, as concerns about a full-scale Russian invasion of Ukraine remain elevated and put negative pressure on future global oil supply.

For technical aspect, RSI indicator 48 figures as of writing, suggesting that upside is preserving some upside strength as the RSI starts to move north. As for the Bollinger Bands, the price move immediately back inside the lower band after moving out of it, which showed that upside momentum could be expected. In conclusion, we think market will be bullish as the rising RSI reflects bull signals. If the pair crosses above the moving average in Bollinger Bands, the upper band will becomes the profit target.

Resistance: 1.2778, 1.2843

Support: 1.2665, 1.2575, 1.2460

Economic Data:

| Currency | Data | Time (GMT + 8) | Forecast |

| GBP | BoE Gov Bailey Speaks | 21:15 | |

| USD | GDP (QoQ) (Q4) | 21:30 | 7.0% |

| USD | Initial Jobless Claims | 21:30 | 235K |

| USD | New Home Sales (Jan) | 23:00 | 806K |