Daily market analysis

June 2, 2021

Daily Market Analysis

Market Focus

US equities edged lower despite upbeat US Manufacturing number came out on Tuesday. The S&P 500 index lost 0.05% with Energy shares led the gain, while Health Care stocks performed the worst. OPEC+ group agreed to gradually ease production cuts in June and July. In accordance with its April decision, the group will allow to supply 2.1 million barrels per day between May and July. The group is also seeking to balance pick up in demand with the possible increase in Iranian output. Iran is in negotiation with six world powers to bring back its oil output at a cost of suspending the nation’s nuclear program.

Financial institutions in Japan must accelerate efforts to prepare for the transition away from Libor as the expiry of the benchmark could affect financial contracts worth trillions of dollars. Akira Otani, the head of BoJ’s financial markets department, stated “we’re no longer at a stage to wonder whether it’s doable or not, we’re at the stage where we have to get it done.” The country will face big challenge at the end of this month with a local deadline for phasing out use of the benchmark in new transactions.

Reserve Bank of Australia kept cash rate unchanged at 0.1%, here are Bloomberg’s key takeaways from RBA’s monetary statement:

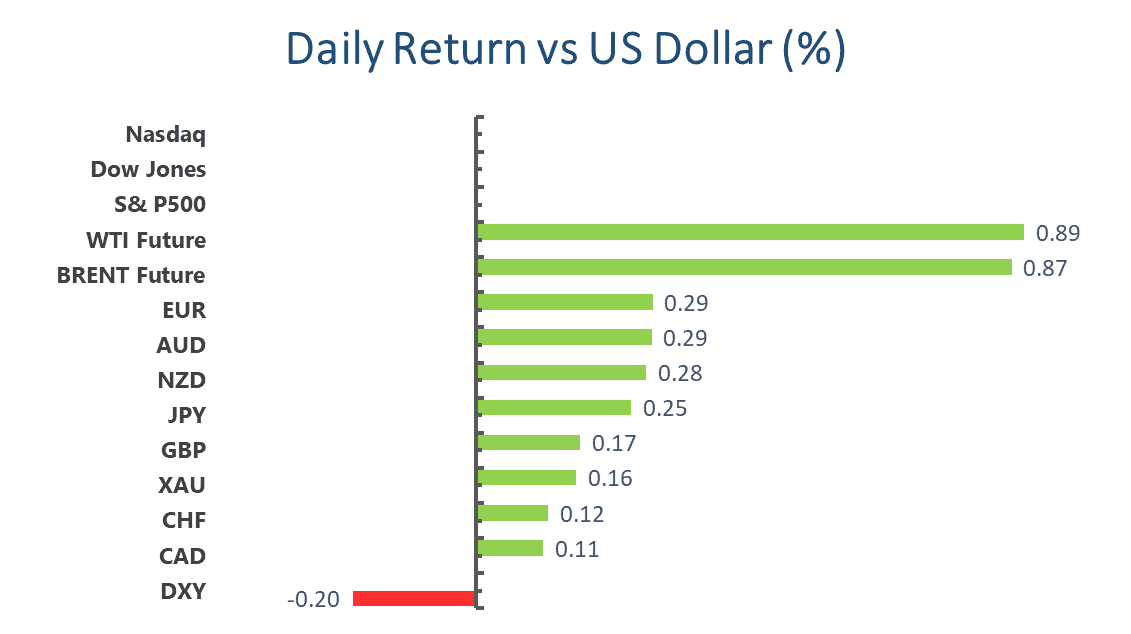

Main Pairs Movement:

Euro dollar climbed as much as 0.23% amid decent German employment data, but all gains was erased later in the day, leaving the pair essentially unfazed. German unemployment numbers declined 15,000 in May, beating forecast of 9,000. The economic activities in manufacturing sector continue to improve in German with Manufacturing PMI came marginally higher than expected, printed 64.4. A similar data came out on the other side of the pond, US ISM Manufacturing PMI ring to 61.2 from 60.7 in April, showing a steady recovery from the pandemic.

Cable tried to break above 1.42 hurdle, but failed to capitalize its earlier gains and closed 0.4% lower at the end of the day. Downbeat Manufacturing PMI in the UK just happened to be the factor weighing down on the Sterling, the figure came slightly under expectation of 66.1, printed 65.6. With concerns of the spreading India variant, UK authorities are speeding up their vaccination campaign, aiming to vaccinate 75% of the population by the end of the month.

Crude Oil look to close above two-year high, Brent and WTI crude futures settled around $71.17 and $68.65 respectively. It is somewhat surprising to see USDCAD is holding up quite well despite rising fuel prices, but still range bounded between 1.2133 and 1.2025.

Technical Analysis:

XAUUSD (Daily Chart)

After 2 mouth’s uprise, XAUUSD seems to be blocked by a cap price out of nowhere. In nearly a week’s consolidation, gold took 3 attenpts to break the $1910 resistence but failed, including the one yesterday, and it traded at $1902.79 as of writing. However, gold remains its uptrend and has backed by its 20-day SMA since mid-Apirl. The fundimentals are still in favor of gold: greanback is still weak, the reflation threat still haunt the whole market, and U.S. pace to recovery is still unclear. Gold may run up toward its upside tractions around $1930, further challenge the yearly top at $1960.

The instant support for gold may be the psycholocial $1900, under that we have 10-day SMA level which is around $1890, followed by 20-day SMA’s $1860.

Resistance: 1910, 1930, 1960

Support: 1900, 1894, 1867

USDCAD (Daily Chart)

Loonie has again broken its record yesterday, once traded at 1.2005, its lowest level in nearly six years. The renewed bearish pressure may derive from the rising oil prices that capitalized the commodity-sensitive CAD, and the contunued weakness of the greenback also add fuel to the bears. Meanwhile, investors is looking forward to the NFP and Canada Unemployment Rate data released on Friday to provide further instructions.

For a possible rebound, the instant resistence may be at 1.215 which has not been breached for two weeks, followed by 1.225, the past support level from February, 2018, and 1.237, the monthly low in March, 2021; however, if the downward trajectory continues, the last baricade for the loonie may be at 1.192, an ancient support from May, 2015.

Resistance: 1.215, 1.225, 1.237

Support: 1.20, 1.192

EURUSD (Daily Chart)

EURUSD has held a bullish tone since the beginning of April, coincided with the start of the greenback’s fall. Recently, the dollar index lingered around its four-month lows, as the Fed’s dovish reaction toward the emerging reflation. Last Thursday, despite Fed implies a tapering discussion at upcoming meetings, but with substantial progress unlikely to be achieved until late 2021, the US dollar continues to behave weaker even after President Joe Biden announced his fiscal 2022 budget, which should be a huge boost to bucks. Back to technical, EURUSD is traded at 1.2215 as of writing, with its upward trend challenged by the resistance level of 1.225. The MACD histogram shows a bull-bear fight, while RSI indicator has not reached the overbought territory, giving the pair more rooms to extend further north. An obvious support for the potential downturn may appear at 1.217, which has been tested several times last week, followed by 1.205, the period low after the Mother’s Day. (U.S.)

Resistance: 1.225, 1.235

Support: 1.217, 1.205

Economic Data

|

Currency |

Data |

Time (GMT + 8) |

Forecast |

||||

|

AUD |

GDP (QoQ) (Q1) |

09:30 |

1.5% |

||||

|

GBP |

BoE Gov Bailey Speaks |

23:00 |

|||||

-

Global - English

-

United Kingdom - English

-

France - Français

-

Spain - Español

-

Portugal - Português

-

Italy - Italiano

-

Germany - Deutsch

-

Turkey - Türkçe

-

MENA - العربية

-

MENA - English

-

Asia - English

-

India - English

-

Indonesia - Indonesia

-

Japan - 日本語

-

South Korea - 한국어

-

Malaysia - Bahasa Malaysia

-

Malaysia - English

-

Philippines - English

-

Vietnam - Tiếng Việt

-

Thailand - ไทย

-

China - 简体中文

-

China - 繁體中文

This site uses cookies to provide you with a great user experience.

By using vtmarkets.com, you accept

our cookie policy.

Start trading with

VT Markets today

![]()

Follow us on:

![]()