Strong quarterly earnings often stir hope. But in the current climate, even an impressive earnings season arrives with a tinge of uncertainty. The S&P 500’s Q1 2025 results were undeniably robust on the surface—12.8% year-over-year earnings growth, 76% of companies beating EPS estimates, and a streak of seven straight quarters of gains. It’s the second consecutive quarter with double-digit growth, a feat that should have been celebratory. Yet, beneath that polish, signs of hesitation are building.

With approximately 72% of S&P 500 firms having reported, earnings have indeed come in stronger than anticipated. Profit margins improved to 12.7%, up from 11.8% the year prior. Revenue also rose, extending its growth streak to an 18th quarter, albeit more modestly at 4.8%, which is still below the 5-year average of 7.0%. Giants in Communication Services and Health Care led the charge, with Meta, Alphabet, Microsoft, and Bristol Myers Squibb outperforming expectations. Their strength helped mask some softness in other areas.

The energy sector, in particular, told a different story. Its earnings shrank by -14.4% year-over-year, largely due to suppressed oil prices. Industrials, too, stumbled, weighed down by contracting revenues. These sector-specific weak spots mattered more than usual this time—because they’re the very areas most vulnerable to what’s coming next.

What to Expect

Looking ahead to Q2, analyst sentiment is growing more cautious. Since March 31, consensus earnings estimates for Q2 have been trimmed by -2.4%. This isn’t an ordinary revision. It’s steeper than the average 5-year (-1.8%) and 10-year (-1.6%) markdowns. The deeper cut reflects growing concerns about margin compression, softer demand, and above all, the looming threat of renewed tariffs. Energy earnings forecasts have been slashed by -14.8%, while Materials have taken an -11.9% hit. Industrials haven’t been spared either.

Only two sectors have seen upward revisions: Utilities, with a modest +0.8% increase, and Communication Services, up by +1.4%. These adjustments are marginal, and they only highlight how fragile forward expectations are across the broader index.

EPS forecasts for the rest of the year maintain a cautious optimism on paper. Analysts expect Q2 2025 EPS to rise by 5.7%, Q3 by 7.8%, and Q4 by 7.1%, with the full-year projection standing at 9.5%. While these numbers still suggest growth, they are clearly losing momentum compared to the 12.8% jump in Q1. This softening trajectory introduces more volatility risk into equity markets, especially if macroeconomic factors worsen.

Despite the softer guidance, the S&P 500 trades at a forward P/E ratio of 20.2—higher than both the 5-year average of 19.9 and the 10-year average of 18.3. This elevated valuation suggests markets are still pricing in resilience through the year and into 2026, where a forecasted 11.1% EPS growth remains on the table. But that pricing makes the index vulnerable to any disappointments, particularly in sectors exposed to global trade.

Analyst ratings remain split. Fifty-six percent of them are Buys, with bullishness still strongest in Energy—despite the steep earnings drop—alongside Communication Services and Information Technology. Price targets across the board indicate a potential 17% upside from current levels. This upside, however, is heavily dependent on corporate America meeting or exceeding those projections in what’s clearly a slowing earnings environment.

For traders, this means watching the Energy sector carefully, as it continues to navigate the twin pressures of lower commodity prices and geopolitical uncertainty. Meanwhile, consumer discretionary and manufacturing firms could also feel the squeeze if tariffs rise and consumer sentiment begins to wane.

Market Movements This Week

With fundamentals starting to wobble beneath strong Q1 results, we shift our focus to what price action can reveal. Markets often move ahead of the narrative, and by studying the key levels and consolidation zones, we can better prepare for what’s next—whether that’s continued upside or a corrective slide.

In currency markets, the US Dollar Index (USDX) has extended its climb from the 98.80 area. With current price action hovering near 100.60, we’re watching for a possible consolidation here. If support holds, the index could stretch further to test 102.00. The dollar’s strength adds pressure to risk assets and commodities alike, especially if investors start pricing in higher-for-longer rates or fresh tariff headwinds.

EUR/USD continues to drift lower, with price now pointing toward the 1.1200 support zone. Should it stabilise here, traders will look for direction into 1.0970 next. GBP/USD paints a similar picture, trading lower and approaching 1.3145 as its next key level. If dollar strength persists, these pairs could remain on the defensive for a while longer

USD/JPY is on the move again, now pushing toward 146.60. If it holds above this level, the next target lies near 149.15. Price action in this pair mirrors broader yen weakness, potentially linked to Japan’s policy divergence and safe haven outflows. The Swiss franc is also weakening—USD/CHF has resumed its upward climb, with 0.8530 now in focus.

AUD/USD, meanwhile, is retesting the 0.6460 area. If price pops higher, bulls may be eyeing resistance near 0.6480 or 0.6520. On the downside, 0.6385 remains the key level to watch. NZD/USD is slightly more active, trading up from the 0.5910 zone. But to see any real momentum, price needs to break above the 0.5986 or 0.6000 levels. If sellers return instead, 0.5870 is the next likely test.

USD/CAD is bouncing off support at 1.3755, a level that’s now acted as a floor more than once. If price turns upward again, traders will be watching 1.3910 or 1.3945 for resistance. If the move doesn’t stick, 1.3710 could be the next magnet. Canadian dollar weakness often rides in tandem with lower oil prices, so the correlation remains in play.

Crude oil remains under pressure. West Texas Intermediate (USOil) continues to trend lower and is approaching the key 58.30 level. A pause or consolidation here could open the door for fresh bearish setups, with 53.00 as the next major downside target if momentum doesn’t stabilise. The decline in oil aligns closely with the earnings contraction seen in the Energy sector, adding further weight to that theme of weakness.

Gold has been quiet, hovering below $3300. If we see a consolidation pattern form, bearish setups could trigger below this level. Gold has struggled to hold higher ground lately, despite global uncertainty and softer central bank rhetoric. This suggests that traders may be rotating out of safe havens in favour of risk assets—or simply waiting for a clearer directional cue.

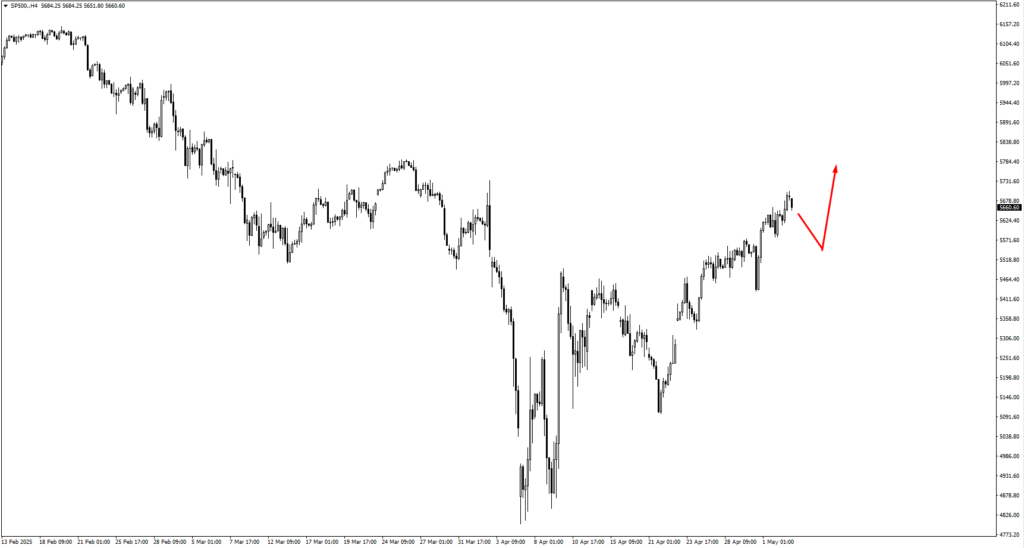

The S&P 500 climbed higher last week, rising above the 5610 level. This rally echoes the optimism we saw in Q1 earnings, but with forward earnings estimates being revised lower, we’re eyeing this move with a bit more scepticism. If price consolidates here, traders may watch for bullish action near 5490 before making a push toward 5775 or 5830. However, failure to hold the 5610 zone could unwind some of the recent gains quickly, especially if macro headwinds intensify.

Bitcoin keeps grinding higher and is now pressing against the 98,300 level. If this momentum holds, crypto bulls could drive price toward fresh highs. However, if we see a pullback, bullish price action at 94,510 or even 91,500 would be the key areas to reassess long positions. With risk appetite flickering on and off, Bitcoin is still acting as a bellwether for broader speculative sentiment.

Natural gas is sitting tight around the 3.50 mark. Consolidation here could set up for a bullish move if price finds strength at 3.30. But with summer demand still unclear and storage numbers in flux, traders may want to wait for a stronger signal before jumping in.

Key Events This Week

With earnings now winding down and macro focus returning, even routine data releases and policy meetings could have ripple effects—especially in a market already wrestling with inflation risks, slowing global growth, and fragile sentiment across key sectors.

On Monday, May 5, the U.S. ISM Services PMI offers an early signal for the week’s tone. The index is forecast at 50.2, down slightly from 50.8. While the difference may look small, anything below 50 marks a contraction. Services have been one of the more resilient pockets of the U.S. economy, so a weak reading here could spark new concerns about the breadth of the slowdown—especially if paired with weaker consumer activity data in the coming weeks.

The spotlight falls on Thursday, May 8, where both the Fed and the Bank of England will take centre stage. The Federal Reserve is expected to hold rates steady at 4.5%, maintaining its current stance amid softening inflation and growing political scrutiny. While no fireworks are anticipated from the rate decision itself, Powell’s tone during the post-meeting commentary could shift risk sentiment quickly. Any mention of tariff impacts or stickier inflation components could renew volatility, particularly with equity valuations sitting above historical norms.

Across the Atlantic, the Bank of England is forecast to cut its policy rate by 25 basis points to 4.25%, a move designed to counteract persistent economic drag. With UK growth struggling and inflation still well above target, the decision may mark a pivot point. If the rate cut is accompanied by dovish guidance, it could weigh further on GBP pairs already under pressure, particularly against a strengthening U.S. dollar.

Then on Friday, May 9, the U.S. Non-Farm Payrolls report will round out the week. Forecasts sit at 129K—well below the prior 228K—while the unemployment rate is expected to hold at 4.2%. This marks a critical inflection point. Another sharp drop in jobs growth could reinforce the narrative that the labour market is finally softening, potentially reviving rate-cut bets. But if the unemployment rate ticks higher, markets could start reassessing the durability of earnings strength in the face of weakening demand.

We’re watching all of this unfold through a cautious lens. None of these events are singular catalysts on their own, but taken together, they could shift the balance of risks—especially in sectors already under pressure from downgraded earnings outlooks. As volatility creeps higher and markets test key technical levels, it’s what’s between the lines in the data and statements that may matter most.